Q&A: Your Money Map

I chatted with Jean Chatzky of Your Money Map about HNTI and some general investing concepts. As always, we did notget to all of them, but they were so thoughtful, I wanted to share them with you. *Let’s start with the why. Many, if not most, investing books aim to teach people how TO… Read More The post Q&A: Your Money Map appeared first on The Big Picture.

I chatted with Jean Chatzky of Your Money Map about HNTI and some general investing concepts. As always, we did notget to all of them, but they were so thoughtful, I wanted to share them with you.

*Let’s start with the why. Many, if not most, investing books aim to teach people how TO invest. Your focus is giving readers advice on how NOT to invest. Why did you decide to take this approach?

Less gullible, more skeptical. We evolved as a cooperative species of Social Primates; we are inclined to cooperate and say yes. It makes us an easy target for slick salesmen on TV and IRL.

*The book is broken down into four categories of things not to do when you’re investing. I’d like to dig into “Bad Ideas” first. These, of course, are the “bad ideas” associated with investing. You say there are three areas where they’re derived from. What are they? What can people do to avoid poor advice?

My organization structure

1: Poor Advice

2: Media Madness

3: Sophistry: The Study of Bad Ideas

Or, where bad ideas come from, how they spread, why they fool us.

*These days, turning on the TV to get the latest news about the markets and the economy can be enough to send anyone into panic mode. You say we “give way too much credit” to the media when it comes to accurately covering financial happenings. Why is that, and how can someone know what to pay attention to and what to tune out?

Example: last week, JP Morgan cutting its price target on Fed Ex from $323 to $280, highlighting weak guidance/outlook; the stock is getting hammered in the pre-market it’s down by 9%

Critical thinkers should look at that broadcast and immediately ask themselves these questions: What’s this analyst’s track record on the stock, the sector, and the market? Should I care about a stock target of 280/323 (it’s 230)? How useful is management guidance? Is it late, early, boilerplate legal noise? Pre-open trading is usually thin and often hits extremes. Does down 9% suggest anything for future performance? What is the track record?

Just because an outlet publishes, broadcasts or posts online does not give them any special insight – and certainly zero clairvoyance.

*You write, “In the world of investing, recognizing what you do not know and therefore should not be betting on is paramount.” Why is this such an important trait for investors to have?

We all engage in behaviors where we imagine our skill level and abilities are much higher than they really are. This is more than overconfidence, the DKE is how poorly we are at metacognition – assessing our own abilities at a specific task

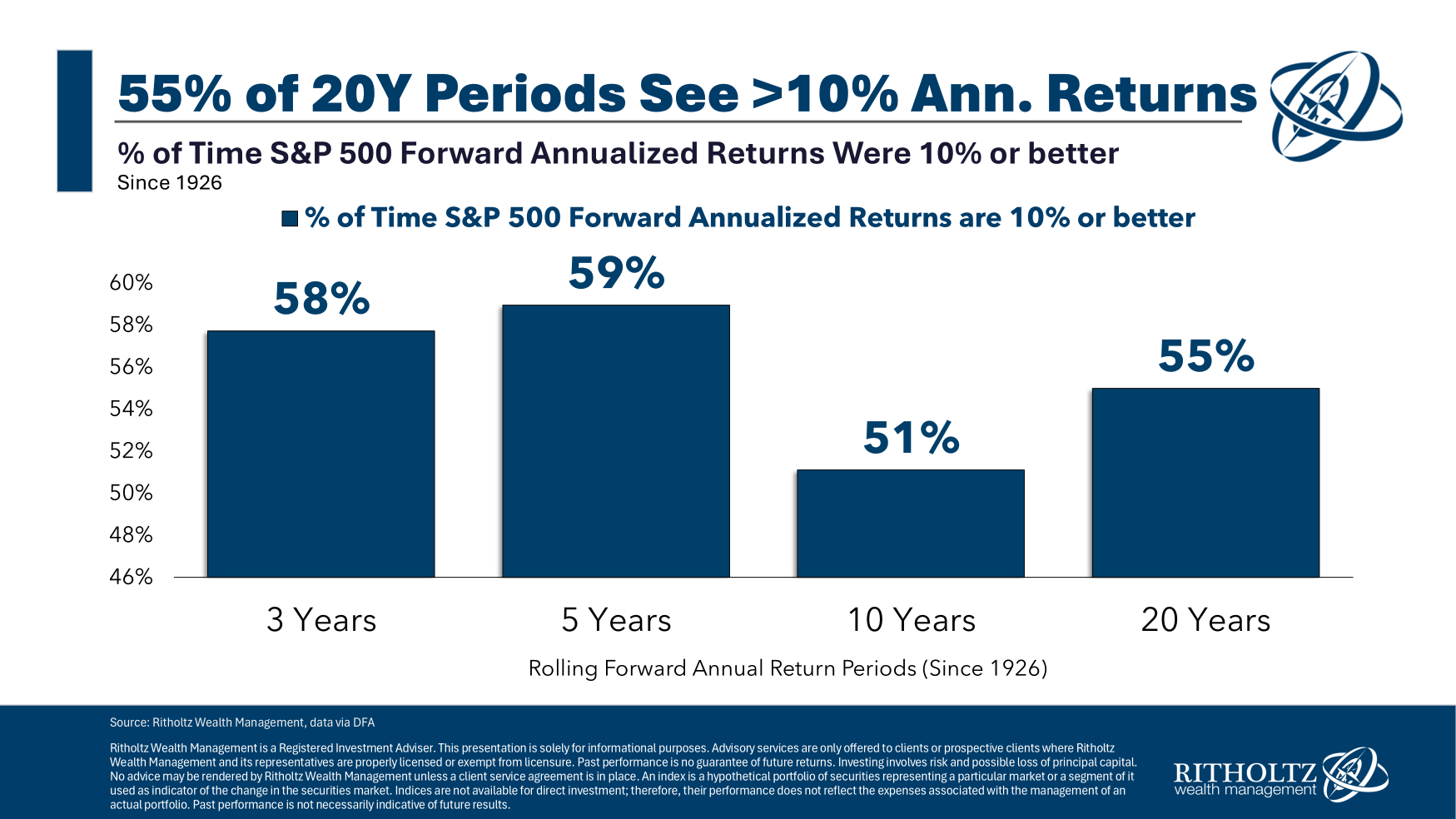

Look at the history of performance and the small number of professional investors who outperform their benchmarks over 1, 5, 10, and 20 years.

*The second section of your book focuses on “Bad Numbers,” or in other words, misleading numbers that could drive the economy, the markets and ultimately, your investments. What are some examples of “bad numbers?”

Compounding, Denominator Blindness, Survivorship Bias all affect our abilities to make good decisions about the future when even basic math is involved.

*You write, “Forecasts of a recession arriving during the next four years are just a waste of print and pixels. The only thing these predictions do accomplish is to remind us that yes, there is always a storm somewhere off in the future.” What do you make of what’s going on right now in the economy? Are the fears many people have about us entering into a recession overblown?

I wrote two posts recently based on what clients where asking. “Tune Out the Noise” told investors to not get to distracted from their plan; I never want to be sanguine or blase about the volatility.

So the follow up was: “7 Increasing Probabilities of Error.” I looked at Recession, Profits, Valuations, US Dollar, Geopolitics, Market crashes. In all cases, the risk levels were rising but off very low levels; they are higher today than before Jan 20 but still relatively low.

So far, its been mostly noise… but the big question is “What’s your timeline?”

If you are retiring in the next 12-36 months, you have a right to be concerned. If you are investing for a purpose 10 to 20 years out, then the probabilities are 47 is a 4-year blip, and you have to look past this.

*You cover the difficulties people have when it comes to finding the right stocks to buy, determining how long to hold onto an investment and then, recognizing when it’s time to sell. Why are these things so challenging for people and what can they do to make them easier?

That’s based on lots of academic studies (There are 100s of endnotes sourcing all of these)

Favorite example: One study found that mutual fund managers were good buyers of stock, but bad sellers.

Explanation: Buying was primarily a quantitative, strategy-based decision; selling was mostly an emotional call. Amazing data, great methodology,(Random sells 50-100 bps)

*The third section of your book focuses on behavioral economics and some of the biggest money management errors you’ve seen people make. What are some examples? How can we change our way of thinking to avoid these missteps?

(How much time do we have?)

So many terrible examples: Advisors became billionaires, trifecta from hell.

Blame Your Limbic System

Risk Is Unavoidable. Panic Is Optional.

*As you’re likely aware, we’re in the midst of “Peak 65,” where we’re seeing more people turning the traditional retirement age of 65 than ever before. How should a person who is approaching retirement NOT invest? How should a person who is already retired NOT be investing?

4 factors: Account size, ongoing contributions, spending, lifespan (Note inflation/market action are not in here)

But its really balancing two things: Longevity vs drawdowns.

*One of the lines in the book that I think will resonate with people, especially now, is “Risk is unavoidable, panic is optional.” What would you say to people who are anxious about their investments today? How should they be reacting to the economic volatility?

What is in your control, what is not?

Stoic philosophy is Control what you can

*The final part of your book is called “Good Advice.” There’s a lot there – one of my personal favorites being your advice to “Buy yourself a f*^ing latte.” What do you think are the three most valuable pieces of financial advice you can give our audience?

I am not a fan of the spending scolds — if a $5 latte stands between you and retirment, you have probably sdone something terribly wrong.

Money is a tool, use it for its best purposes. Beyond Maslow’s hierarchy of needs and Investing, there is a lot of things you can use money for: Buy time, buy experiences, create memories with frewinds and family.

Audio below

The post Q&A: Your Money Map appeared first on The Big Picture.