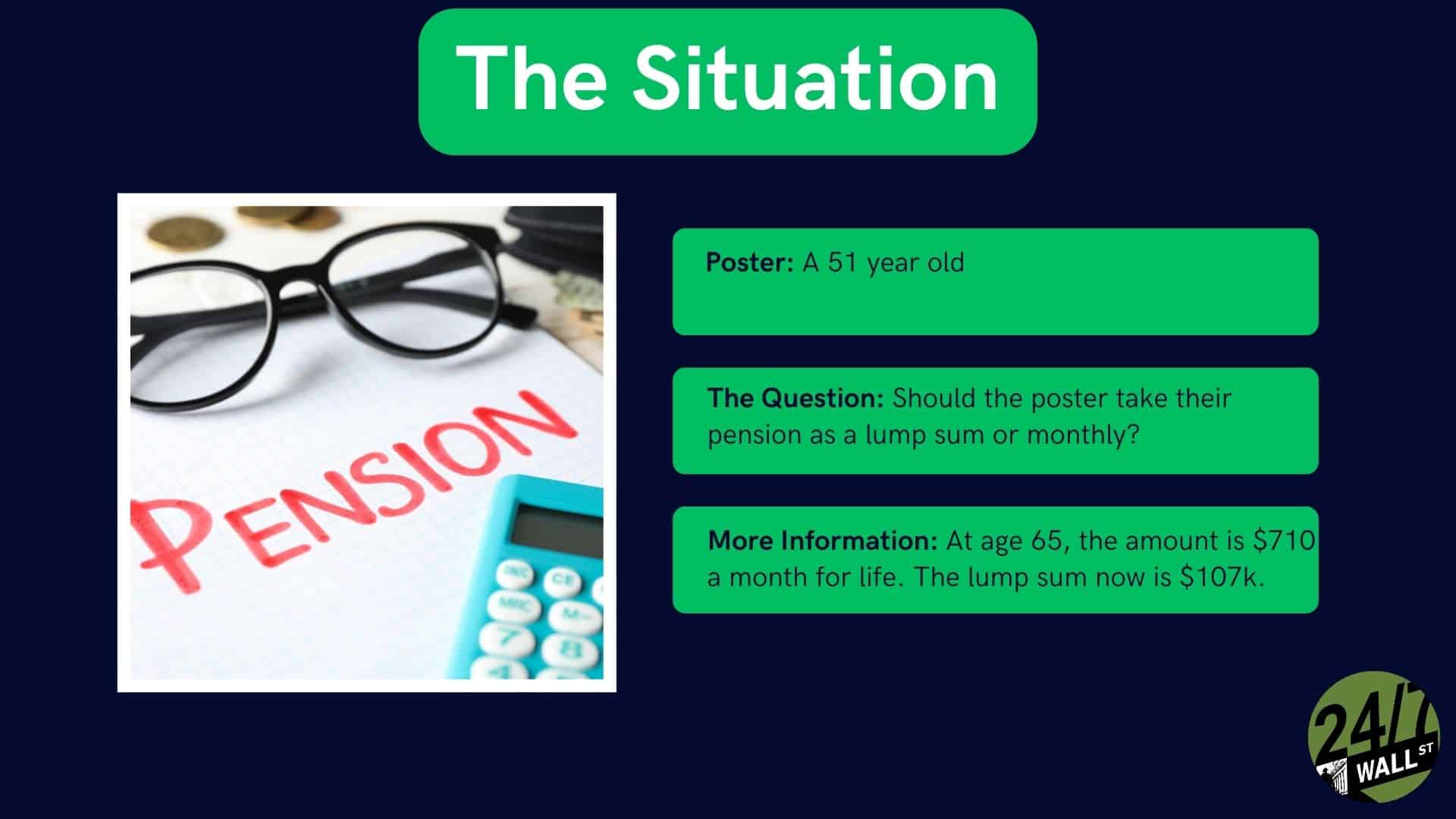

I’m 51 and debt-free – is it smarter to take a $107K lump sum or $710 monthly pension when I retire?

Should you take the lump sum or receive monthly payments from your pension? It’s a question many people ponder, and some of those people take the time to post their thoughts in the Dave Ramsey Reddit group. This post comes from a 51-year-old who can take a $107k lump sum or receive $710/mo for life. […] The post I’m 51 and debt-free – is it smarter to take a $107K lump sum or $710 monthly pension when I retire? appeared first on 24/7 Wall St..

Should you take the lump sum or receive monthly payments from your pension? It’s a question many people ponder, and some of those people take the time to post their thoughts in the Dave Ramsey Reddit group.

This post comes from a 51-year-old who can take a $107k lump sum or receive $710/mo for life. Both of those options seem to become available when the Redditor turns 65, based on OP’s responses to some of the comments.

I’ll share my thoughts, but it is always good to speak with a financial advisor if you can.

Key Points

-

A Redditor is deciding between a $107k lump sum or $945/mo payouts from a pension.

-

We need more information to make a better assessment, but most commenters recommended the lump sum.

-

Are you ahead, or behind on retirement? SmartAsset’s free tool can match you with a financial advisor in minutes to help you answer that today. Each advisor has been carefully vetted, and must act in your best interests. Don’t waste another minute; get started by clicking here here.(Sponsor)

The Advantages of Monthly Payouts

Monthly payouts are more beneficial for people who live longer and can quickly burn through the lump sum. If you spend all of the lump sum, you won’t have the safety net of monthly payments.

It would be good to know the Redditor’s portfolio amount and projected Social Security payments to see how beneficial the monthly payouts would be. Monthly pensions make more sense if the $710/mo is critical to covering living expenses. However, it isn’t as valuable if Social Security and small IRA withdrawals are enough to cover monthly expenses.

Monthly payouts offer more stability and less risk. You don’t have to worry about how the stock market performs since you can always count on receiving $710/mo.

The Advantages of Taking the Lump Sum

The lump sum gives the Redditor more money right now, and if you put it in a good ETF, it can grow at 5%-10% each year. That’s a wide range because the optimal ETFs depend on the Redditor’s risk tolerance. It’s hard to gauge the individual’s risk tolerance since we have no information about their financials, living expenses, or long-term goals.

A lump sum can outperform the monthly payouts if you get a good ROI, but there is an added perk. If you receive the lump sum, you guarantee a good inheritance for your heirs. It’s entirely possible for the Redditor to receive monthly payouts and pass away one year later. That doesn’t leave much of an inheritance since the monthly payouts don’t get inherited.

Part of the assessment is anticipating how long you will live. It would take 12.5 years for $710/mo payouts to add up to $107k. That does not include inflation, which is less favorable for the monthly payouts.

What Should the Redditor Do?

It’s hard to offer a definitive answer. While the lump sum can be more beneficial, we don’t know enough about the Redditor’s finances, goals, or risk tolerance to gauge which option is better. Lump sums eliminate the risk of passing away early by ensuring your heirs get a good inheritance.

The monthly payouts might be better if the Redditor lives into their 80s, but even then, the lump sum can outperform the monthly payouts. Part of it depends on how long the Redditor can pay for living expenses with their Social Security and other income sources before having to tap into their pension funds.

Most of the commenters recommended that the Redditor take the lump sum and invest it for a higher return.

The post I’m 51 and debt-free – is it smarter to take a $107K lump sum or $710 monthly pension when I retire? appeared first on 24/7 Wall St..