My Retirement Savings Are Lacking – Am I Counting on Inheritance or Government Support?

It should go without saying that in today’s day and age, it’s perfectly normal to be concerned about whether or not you are setting enough aside for retirement. The hope is that you can set aside money while working so that you can both live comfortably and prepare for your golden years. This is the […] The post My Retirement Savings Are Lacking – Am I Counting on Inheritance or Government Support? appeared first on 24/7 Wall St..

It should go without saying that in today’s day and age, it’s perfectly normal to be concerned about whether or not you are setting enough aside for retirement. The hope is that you can set aside money while working so that you can both live comfortably and prepare for your golden years.

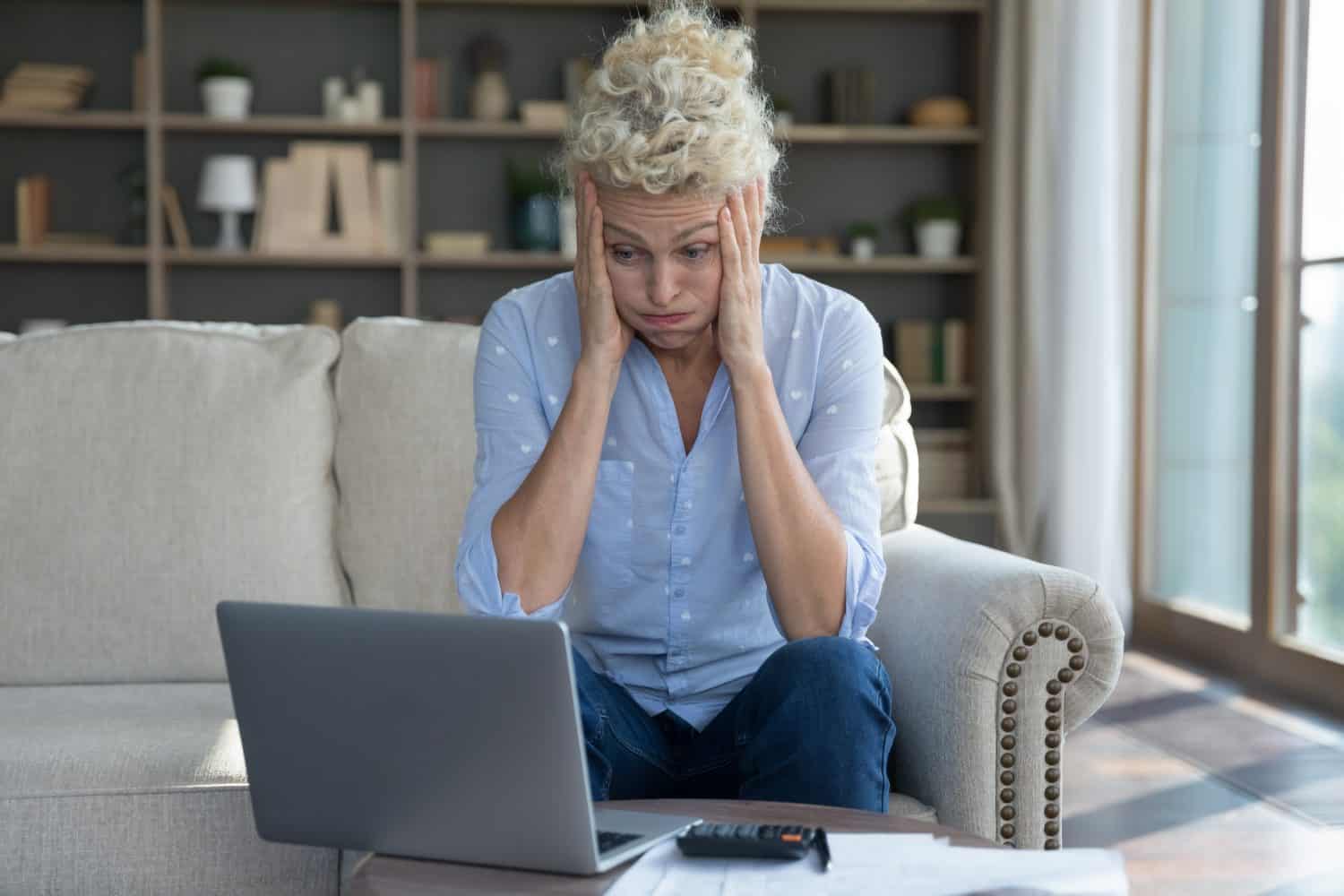

This Redditor is growing increasingly concerned about retirement and not having enough to get by.

This problem is growing in numbers as more and more people struggle to set aside savings.

There is a question about how some people are navigating a shortfall

Key Points

This is the exact question one Redditor is asking in a post on r/MiddleClassFinance, as they are worried about whether they have enough savings for retirement. As a result, they are asking fellow Redditors how they are planning for any eventuality in which they don’t have enough.

Not Saving Enough

There is no question that as you get older and closer to retirement, it’s perfectly normal to feel some pressure about where your savings are for your age. In this Redditor’s case, they are trying to understand how others are catching up and figuring out how to live financially after retirement.

This leads directly to the original poster asking if other redditors are counting on an inheritance, support from their children, working forever, or government support? They also wonder if people will relocate to areas with a lower cost of living.

When you consider that the average savings of a household ages 45-54 is just $313,200, $537,560 for 55-65, and only $609,230 for between 65 and 74 years of age, it’s understandable why people are concerned. While these numbers from Edward Jones might sound like a lot on the surface, it’s far less money than most people need to retire.

How Much Do You Need?

As one of the biggest names in the finance world, it’s worth taking Fidelity’s advice on what you need to retire. For its part, Fidelity suggests that most people should have at least 10 times their highest annual salary saved for retirement before retiring. In other words, if you make $100,000 per year, then you should need at least $1 million set aside for retirement. The challenge is that most people aren’t anywhere near this number, which is exactly why this Redditor felt it necessary to ask a question about how those who are well-off are managing their finances.

What Kind of Support?

While many people are counting on Social Security, which is exactly the type of government support this Redditor is hinting at, it raises the question of what happens if Social Security isn’t in a good place. As it stands today, Social Security payments are expected to start being reduced by 2035, as the program’s solvency remains an issue due to fewer workers contributing to the trust fund than in decades past. At best, Social Security is only support to replace as much as 40% of pre-retirement income, so it’s definitely not a solution for most people.

Separately, even if baby boomers pass on the greatest amount of wealth in history to their children, this doesn’t mean everyone stands to benefit. Taxes and unnecessary spending habits could easily reduce the amount of money most people have for retirement after their inheritance is finalized.

In the comment section of the Reddit thread, it is clear that many people intend to relocate to a lower-cost-of-living area, but also work significantly longer than originally expected. The hope is that most people can retire when they reach Full Retirement Age at 67.

Unless you have a pension or significant money set aside, even getting Social Security at this point with middling savings won’t be enough to sustain a good lifestyle. Things worsen if there are any unexpected medical expenses, which is arguably the greatest financial concern for most people during retirement, especially before they can take advantage of Medicare.

If you are not working with a financial advisor, now is a great time to meet with one to discuss your goals and options. This is also a great time to make sure you are taking advantage of employer-matching 401(k) funds, which are essentially “free” money that you can use for retirement.

The bottom line is that people who feel stuck without sufficient savings to retire will either place a significant financial strain on their children or rely on government support that may not exist in the same form as it does today. This is a challenging position to be in, and there is no straightforward solution to quickly build up savings.

The post My Retirement Savings Are Lacking – Am I Counting on Inheritance or Government Support? appeared first on 24/7 Wall St..