My husband and I have been shoveling money into retirement accounts with the goal of retiring in 20 years – how should I factor inflation into our plans?

The FIRE (Financial Independence Retire Early) ethos contains several principles, but is fairly agnostic as to the methods of achieving goals according to those principles. Whether an individual is anticipating a sizable pension, owns real estate for ancillary income, has company stock in their 401-K, or holds other assets, anyone who embraces the FIRE approach […] The post My husband and I have been shoveling money into retirement accounts with the goal of retiring in 20 years – how should I factor inflation into our plans? appeared first on 24/7 Wall St..

The FIRE (Financial Independence Retire Early) ethos contains several principles, but is fairly agnostic as to the methods of achieving goals according to those principles. Whether an individual is anticipating a sizable pension, owns real estate for ancillary income, has company stock in their 401-K, or holds other assets, anyone who embraces the FIRE approach can craft their own strategy based on individual available resources.

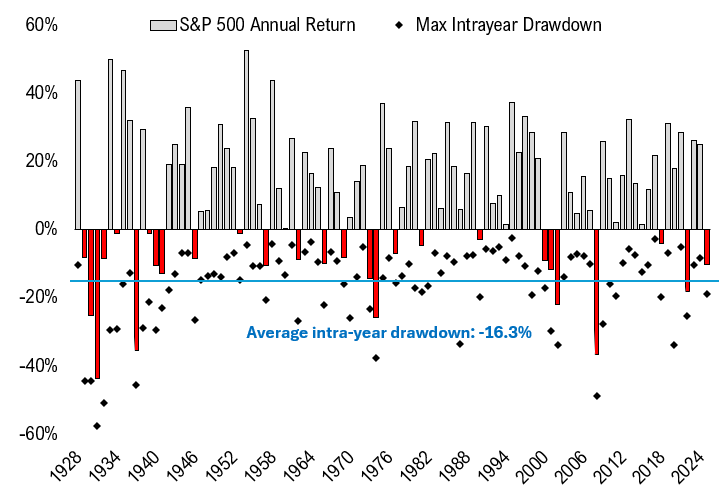

This DIY approach is part of the FIRE and fatFIRE appeal to Millennials and Gen-Z, and a slew of forum tips, calculation formulas, and other hacks have proliferated. However, many of the models used by FIRE adherents can be overly optimistic, such as a popular rule of thumb 4% safe withdrawal rate (SWR) per year. Even Bill Bengen, the creator of “The 4% Rule”, later revised it as the 4% figure was based on a bull market, low inflation period during the 1960s. Bengen noted that 4% was not representative of subsequent inflation reaching the highs of the Biden and Carter years, and for bear market conditions, such as the dotcom bust and the 2008 subprime mortgage banking meltdown.

Key Points

-

Factoring inflation into one’s FIRE calculations requires guesswork, so overestimation towards a more conservative SWR is advisable.

-

457b tax-deferred plans, which are available to municipal employees, differ in several ways from private sector 401-K plans.

-

Other tax-deferred savings, such as HSA and 529 accounts, should be factored into a comprehensive savings plan for the family.

-

Are you ahead, or behind on retirement? SmartAsset’s free tool can match you with a financial advisor in minutes to help you answer that today. Each advisor has been carefully vetted, and must act in your best interests. Don’t waste another minute; get started by clicking here.(Sponsor)

Inflation Fears

A doctor in her 40’s and her husband have embarked on a FIRE path. In the course of her calculations to determine what size nest egg for retirement will meet their FIRE retirement goals, she found herself stuck on how to properly mathematically account for inflation. She decided to post on Reddit for advice on that and to solicit other suggestions. Their profile contains the following:

- Poster is 41 and recently increased her annual salary from $250,000 to $450,000+. All of her medical school loans have been paid off.

- Her husband, 45, earns $80,000 annually.

- They would like to retire in 20 years.

- Their savings rate has been 15%-20% annually, invested in Vanguard target date index funds.

- Current savings is $750,000 – all in deferred 401-K and 457b accounts. (457b accounts are municipal employee retirement accounts. They don’t have an under age 59.5 penalty, and allow for one to make “catch-up” contributions in yars in which they might have skipped earlier.)

- The couple also have an underfunded 529 account for their (2) elementary school aged children.

- Based on a 4% $200,000 annual SWR, the poster calculates needing a FIRE target of $5 million.

- The poster and husband are presently saving more than $100,000 per year, at $8,500 per month. She calculates that at 6% interest, they will have $5.7 million in 20 years.

The poster’s primary concerns and questions are:

- How does one factor inflation into the equation, and won’t that render $5.7 million insufficient for their FIRE plans?

- Should her raise and increased savings amount be invested in a more strategic vehicle than the Vanguard target date index funds holding the present savings?

- Should the additional $100,000 in savings be allocated to a taxable account, and is there an advantage to adding a Roth account in conjunction with, or to rollover from the current tax-deferred ones?

Inflation, Taxes, and Job Satisfaction

The Reddit responses contained several helpful tips and observations for the doctor and her husband, such as:

- Kudos for choosing the 6% growth rate. Most calculations are based on the performance of the S&P 500 over the past two decades, average growth at 10%. By reducing to 6%, that is a safe margin to accommodate average inflation and arrive at a SWR.

- The higher tax bracket bump from her salary increase will likely necessitate a FIRE target of $6 million to $7 million for her $200,000 SWR.

- In general, brokerage and Roth accounts offer more flexibility in dealing with taxes than traditional 401-K accounts.

- One respondent advised establishing a Health Savings Account (HSA), which may be crucial for the couple in the future.

- Also recommended was establishing a Back Door Roth IRA, which involves making non-deductible contributions to an IRA and then converting them to a Roth IRA. This bypasses the income limit eligibility cap.

- One commenter noted how child care costs might be a factor, but the doctor explained that her husband loves his job, since it is also his hobby. Therefore, it gives him maximum flexibility to be a stay-at-home dad while earning a good wage while she tends to her patients, so child care expenses are a moot issue.

This article is written from an informative perspective. Anyone seeking more in-depth financial advice should consult a financial professional.

The post My husband and I have been shoveling money into retirement accounts with the goal of retiring in 20 years – how should I factor inflation into our plans? appeared first on 24/7 Wall St..