Transcript: Sander Gerber, CEO and CIO Hudson Bay Capital

The transcript from this week’s, MiB: Sander Gerber, CEO and CIO Hudson Bay Capital, is below. You can stream and download our full conversation, including any podcast extras, on Apple Podcasts, Spotify, YouTube, and Bloomberg. All of our earlier podcasts on your favorite pod hosts can be found here. ~~~ This is Masters… Read More The post Transcript: Sander Gerber, CEO and CIO Hudson Bay Capital appeared first on The Big Picture.

The transcript from this week’s, MiB: Sander Gerber, CEO and CIO Hudson Bay Capital, is below.

You can stream and download our full conversation, including any podcast extras, on Apple Podcasts, Spotify, YouTube, and Bloomberg. All of our earlier podcasts on your favorite pod hosts can be found here.

~~~

This is Masters in business with Barry Riol on Bloomberg Radio.

Barry Ritholtz: Strap yourself in for another good one. Sander Gerber, C-E-O-C-I-O of Hudson Bay Capital. What a fascinating background he has, starting in philosophy and ending up on the floor of the American Stock Exchange as an equity options trader. That experience those two things combined to really create a kind of unique perspective on the world of markets, on the world of risk, and on the world of models. You know, I’ve used the George Box quote a million times, all models are wrong, but some are useful. And the way Gerber goes about using models is very much along the George Box lines, which is not only are we gonna assume that models are wrong, but we want to create our own models to be able to identify when they’re gonna be at a great variance to what’s going on in reality, and then how to position ourselves to take advantage of it. They’re less directional traders than they are Arbitrages. Hudson Bay Capital runs, you know, a dozen different strategies and they’re all quite fascinating. Everything from risk arb to private credit and real estate in the first quarter of 2025, where volatility spikes and a lot of people’s expectations are dashed. Their models do really well. I, I find his depth of knowledge and his technical expertise to be absolutely fascinating. I think you’ll find him to be fascinating. Also, with no further ado, my conversation with Hudson Bay Capitals, sander Gerber.

Barry Ritholtz: So let’s start a little bit with your background. Bachelor’s in Humanistic philosophy and an MBA from Wharton Finance. What was the career plan?

Sander Gerber: Well, actually I was good at math. So I first entered the Wharton School undergrad. I don’t have an MBA from Wharton. And then when I was at Wharton, I didn’t think I was getting an education, so I decided to transfer into the College of Arts and Sciences. So I got two degrees concurrently. I picked up a degree in philosophy, humanistic philosophy. I wanted to understand the development of thought, how we got to where we are in society,

Barry Ritholtz: Epistemology, or something more specific.

Sander Gerber: It was more philosophy generally, starting with the ancient Greeks through the existentialists. I think that I use my philosophy background much more than my finance background because it really gives you a different view on the world. When I was at Wharton College, Andrew Krieger came in 1987 to speak. He had majored in Sanskrit Eastern philosophy, and then he got his MBA at Wharton, and he was the leading FX trader at Bankers Trust. And he spoke about how his philosophy, eastern philosophy, helped him understand the markets that you might feel very convicted, the markets should go a certain way, but the markets have their own mindset and you have to accept what the markets have. And it helped him emotionally to trade better because he realized that mother markets was gonna be right. And so it was from his philosophy background that he was able to reconcile that with him, with his beliefs in terms of where markets should go, and it helped him to be a better trader.

Barry Ritholtz: I definitely can see that, you know, the concept, I dunno if I’m stealing this from Zen Buddhism, but it’s the water flows, but the rigid tree breaks in the storm. Huh. And it’s very similar to hey, that, that’s a Eastern way of saying why are you fighting the trend?

Sander Gerber: Exactly. And, and so, you know, when I was in college, I, I really didn’t know much about the markets. And as I told you, I, I still, I had entered first the Wharton School, so I was still getting my degree there, but I was really focused on the philosophy and, you know, people think the philosophy’s not so practical, what are you gonna do with it? And here are the top FX trader in the world came and said, this is what you should be doing. So it was, it was sort of, you know, ratification of, of what I was studying. Huh.

Barry Ritholtz: I think you’re the first person who I’ve ever spoken to who said, yeah, the Wharton School of Finance at University of Pennsylvania. Not a great education. I, isn’t it really true that most of our education, or at least for a lot of people, you’re just self-taught, schools will give you a curriculum and here’s the reading list, but it’s up to you to kinda learn whatever there is to learn.

Sander Gerber:I think it’s a good point. You know, the Wharton School is arguably the finest finance school, but finance is a technical discipline. And I wanted to understand the world. And I think that you can only go a certain degree using that background. And it’s true that in order to, I think upgrade yourself, you’ve gotta be able to develop the capacity to self-learn, to take in from the environment around you to enable yourself, to grow your skillset through your experiences, through working with others. And that’s something we try to incorporate within Hudson Bay, is the ability for people’s careers to develop. And it is something that you have to rely on self-learning. And within college, in certain disciplines in college, like in philosophy, a lot of it is, you know, discovery, self-discovery. In other disciplines, there is no self-discovery. So I think it is important to the humanistic background.

00:05:58 [Speaker Changed] So you come out of, out of Wharton and University of Pennsylvania, you start your career on the floor of the American Stock Exchange as an equity options market maker. That had to be a fascinating experience, especially 1990s and two thousands. That was a hot period in option trading. Tell us a little bit about that experience.

Sander Gerber: Well, actually, when I graduated Penn, I had been, I’d clerked on the floor of the Philadelphia Options Exchange in 1987. And I liked it, but my parents had spent all this money to send me to a fancy school. They had taken out a home equity loan to pay for my college tuition. So I thought to be a measly floor trader would be disrespectful. So I went to Bain and Company for two years, and I was in management consulting for two years. It was boring, but I did learn something from it. And then I came to the floor of the amex.

Barry Ritholtz: Wait, before You jump to the Amex, aside from learning that Bain was boring, what else did you learn?

Sander Gerber:I learned how people can work together in good conscious with dedication and still muck things up. Because what we would do is we would parachute into places like British Airways, Montreal Trust Ca Industries, and we were like the external strategic planning. And we, we would, they would put young people like me and we’d sit next to people and interview them and figure out why projects went to Muck. And I understood from that that well-meaning people can still muck things up because they don’t have an appropriate guide frame or appropriate leadership, or they’re not, so like little things can take projects astray. So

Barry Ritholtz: What was it that drew you to the floor of,

Sander Gerber: Of the, well, I’d enjoyed the Philadelphia floor, and also I was, I always liked games. And so I, and I had a talent I thought for, for trading. And so I went to the, the Amex someone gave me, it was like $1,100 a month as a stipend. And I kept roughly half the profits and there was no training. They just threw me there,

Barry Ritholtz: Throw you in the deep end of the pool, who doesn’t, whoever doesn’t drown. Hey, congratulations.

Sander Gerber: That’s exactly right. Exactly right. And it took me from July of 91 till December of 91, I made $500. Oh my God profit. Not, not for me, $500 trading profit.

Barry Ritholtz: Which you then had a split,

Sander Gerber: Which I had to split. Yes. Well, actually, because I had a draw, I didn’t get anything. But then the next year I took off and it turned out that I, I did have a knack for it. I was able to understand the volatility of the markets, usually we’re all traders. And I, I did something that was two things that were novel on the floor. The first is I understood that you have to break down your volatility exposure month by month, which back then was unusual. In other words, people had these models that would give you one volatility exposure across the entire portfolio. And I realized that July’s an earnings month and August is a beach month, so you can’t use those two months to offset each other. And so I was able to jerry rig the models that were early then to be able to look at my Vega exposure month by month. That was, believe it or not, unusual. And the second thing that, that’s

Barry Ritholtz: Early nineties? Yes. Is that,

00:09:29 [Speaker Changed] Yes, that was 91, 92, 93. Okay.

Barry Ritholtz: It, it, all these things we kind of take for

00:09:34 [Speaker Changed] Granted today. I know,

Barry Ritholtz: Right At one point in time you, you wonder why it’s become so increasingly difficult to beat the broad index. There was a ton of inefficiencies back

00:09:42 [Speaker Changed] Then. That’s right. That’s right. And it was a great edge for me to come to that realization. And maybe it was because I had studied the models at the Wharton School. We had broken them down and I understood that the models are only as good as the inputs. And a lot of people back then were doing spreads in their head. And the other group were using these canned models that would give you one volatility exposure across, you know, the entire model. And the second thing that I realized was that you need to combine fundamentals with the, the technicals of the models. In other words, the models assume a normal distribution of returns, but when you get into some kind of event, it’s no longer a normal distribution returns. It’s, you know, the stock’s either gonna go up a lot or down a lot. That’s a barbell distribution. Right. As opposed to normal distribution. And so by looking at events and when they’re going to happen and breaking down the Vega exposure month by month, that gave me an edge that I was able to exploit.

00:10:46 [Speaker Changed] Define Vega for listeners who aren’t option.

00:10:48 [Speaker Changed] Vegas Vega is the volatility. So vol of o of the op, an option has premium, and that premium is the extra amount you pay for the right to have limited loss and unlimited gain. And so that premium, that value of that option to exercise or not exercise with limited loss goes up and down in value based upon the degree of movement. So when something’s moving around a lot, that has a lot more value. So premium value goes up when things are not moving a lot, premium value goes down. And so by trading this range of volatility up and down, which is in part dependent on what’s happening with the fundamentals of the stock, you are able to grab edge.

00:11:37 [Speaker Changed] So these are really second or third level derivatives. It’s not the underlying value, it’s the increase in value of the option. And then within that, the range of, and the variability of that increase in option value, that’s what you were trading?

00:11:53 [Speaker Changed] Yes. And you know, it’s really not complicated. I mean, wall Street tries to make things much more complicated than they are, but the simple elegant solution is always better. So it might sound complicated, but it’s really not. Right.

00:12:09 [Speaker Changed] That, and that complexity is a feature, not a bug. You can sell stuff if it’s complicated and hard to understand. If it’s simple, well, I think I could do that much. That’s

00:12:19 [Speaker Changed] Right. Wall Street tries to make things more complicated because it has to justify the, the sales commission and if, but things really are not so complicated.

00:12:28 [Speaker Changed] So what was your biggest takeaway from your experiences as a trader? How did it shape how you look at the world of investing? How did it affect what, what you’re doing at Hudson Bay today?

00:12:41 [Speaker Changed] Well, I, I really was grounded by that three and a half years of watching every tick on the stock. You know, and your, you are geographically limited on the floor. You can only trade at the post that you’re standing by, like

00:12:54 [Speaker Changed] Physically in space, physically, you’re,

00:12:57 [Speaker Changed] You’re physically,

00:12:57 [Speaker Changed] You’re tethered to that trading post. Exactly.

00:13:00 [Speaker Changed] And there are even rules that you had to do most of your trading in that geography. So you couldn’t move around a lot. And what it taught me is that, you know, like a trading post, a strategy goes in and out of favor. And if you want to be able to make money in all markets all the time, you have to develop a toolkit that can go beyond one particular strategy. So you need to have multiple strategies to develop persistent profitability. The other thing that I learned was that you can make the right decisions and still lose money. I had plenty of times where looking back it was the right decision, but the markets thought differently. And so you always have to be worried about what can go wrong. And risk is not about not losing money. Risk management is not about not losing money. Risk management is about unexpectedly losing money. In other words, when you are evaluating a situation, you should know what is your reason. Worst case downside. Now there’s always the, you know, black swan that maybe you can’t figure on, but you should. But risk management is always about understanding what could go wrong and quantifying what could go wrong.

00:14:14 [Speaker Changed] So I wanna unpack what you just said ’cause it’s filled with goodness. First you’re referring to your approach is, hey, we’re really more process focused than outcome focused. Yes. Because if you have a good process, even if you get a bad outcome, it doesn’t matter. Probabilities will eventually work in your favor.

00:14:35 [Speaker Changed] That’s exactly right.

00:14:36 [Speaker Changed] That that’s number one. But then the part two, which I think a lot of investors overlook is, and a risk management component that if the worst case happens, we still survive and lift to trade another trade.

00:14:50 [Speaker Changed] That’s right. Exactly right. And so at Hudson Bay, I created the deal code system. Deal

00:14:57 [Speaker Changed] Code system,

00:14:58 [Speaker Changed] Yes. So at the time, well, I left the floor beginning of 95 and started deploying just the money I’d earned on the floor in off floor trading account. And I would develop a strategy and hire someone else to run it and develop another strategy and hire someone else to run it. And as I was having other people manage basically my trading account, I realized I had to scale my risk profile that I developed on the floor over multiple risk takers. And I needed to do it in a manner that would produce persistent profitability. So at the time we were trading a lot of risk arbitrage deals. So we called it a deal code. And a deal code is just a numerical moniker that we put on each trading idea within the book. And that enables us to focus in on how is that trade hedged, what’s the risk riskiness, how much could that trade lose in a reasonable worst case scenario? And it gives us a batting average so we can understand is a portfolio manager winning more ideas than they lose. So to be persistently profitable, I think it’s not just about winning more dollars than you lose, it’s about winning more ideas than you lose.

00:16:12 [Speaker Changed] So let’s talk a little bit about Hudson Bay’s strategy. You’ve been managing outside capital across a variety of asset classes and strategies. Tell us, talk about some of the key strategies and and what has been the drivers of, of making those strategies successful?

00:16:33 [Speaker Changed] Well, as I mentioned, I wanted to be able to make money in all market environments. So you need a tool set to do that. So our strategies are equity, long, short, converts, credit event merger, volatility trading.

00:16:48 [Speaker Changed] This isn’t just, I’m gonna buy the s and p 500 and put it away for a decade. You’re active traders and you’re really looking to take advantage of situations where you have a fairly good idea of what the outcome’s gonna look like. It’s not, hey, this is open-ended. Usually you’re pretty confident in here’s what our range of potential

00:17:09 [Speaker Changed] Outcomes look like. Well, I think that especially in today’s world, you have to understand what your edge is versus the machines. And a machine can calculate risk based on historical precedent, but a machine cannot calculate risk based upon some kind of uncertainty due to some kind of event catalyst or change that’s coming up because it’s new. So the machine doesn’t have the ability to calibrate for something that’s new. And so generally across all our strategies, that’s what we’re focused on is we’re focused on event callous change. How can we profit off of that in a way that machines cannot?

00:17:45 [Speaker Changed] So that’s the fundamental criticism of models. All models assume that the world in the future is gonna look like the world in the past. Risk management is what happens if the world doesn’t look like how it

00:17:57 [Speaker Changed] Used to. Precisely. And, and that’s why we don’t use the standard risk management models. I actually created a statistic that Gerber statistic that helps to understand diversification between our deal codes, between our investment positions. A lot of our competitors are tied to factor-based modeling, which ultimately underneath it is reliant on regression analysis. Regressions are straight line fits through normalized sets of data. And human relationships don’t follow straight lines. And certainly market relationships don’t follow straight lines. So using that as the underpinning of a risk management system is just incorrect. And so we’ve created a, a whole different structure that, as I said, we’ve used since 1998. And I think that’s given us the ability to weather storms and profit from it in ways that our competitors can’t.

00:18:52 [Speaker Changed] So, so let’s talk a little bit about the Gerber statistic. You had this validated by Harry Markowitz, the, the creator of Modern Portfolio Portfolio Theory. Tell us about that collaboration and break down the Gerber statistic a little bit. How, how do you guys actually use it?

00:19:13 [Speaker Changed] So I, because of my distrust of models based upon my experience on the floor, in particularly the guts of the models, I, I never believed in the correlation statistic that correlation is predictive. And this was, I thought, one of the underpinnings of modern portfolio theory that you look at the expected return of the stock, the expected variance of the stock, and the co variance or correlation between the different components of a portfolio. And at the time, you know, we used the deal code system and on Wall Street the banks were telling me, this is nonsense, we don’t even talk about it with investors. And then in oh eight when everyone lost money and we made money, I realized we were doing something different. And then I had the idea of his, of course I’d studied about Harry and modern portfolio theory. Everyone in finance has, he won the Nobel Prize.

00:20:07 I decided, you know what, I’m gonna go out to see him, to see what he thinks about the Gerber statistic. And at the time, it wasn’t called the Gerber statistic, but a friend of mine said, gee, you really should file a patent on this before you see Harry. And so I did, and I had to name it something. So I called it the Gerber statistic, and we now have, I think we just got our sixth patent on our process for diversification. So I gotta see Harry in San Diego, lovely guy. He welcomed me and we’re walking. He liked, he liked to walk along the beach. And I said, Harry, you know, I don’t think that correlation’s predictive. And Harry said, you’re right. I said, no, no, no, Harry, you don’t understand. I don’t think that because this is one of the base foundational bases for which he won the noble prize in modern portfolio theory.

00:20:52 He said, Harry, I don’t think that historical correlation has relevance to the future. And he said, you’re right. And it turns out that in his 1952 paper that sets forth modern portfolio theory, he said that correlation should be determined by the judgment of practical men. In other words, the stock analyst should think what will be the relationship going forward, not to mine the past, but be forward looking. But in the 1960s as computing power increase, people said, oh, we can mine this statistic, this row statistic correlation, and then we can plug it into the model as correlation. He meant correlation in a semantic sense, not in a mathematical sense in terms of using in his model. So he actually said that the deal code system uses his system, the modern portfolio theory system. He, he, he said that there’s three legs to his system. And so because we use limited loss, because we seek to diversification through hedging of the own, because we seek to win more than we lose in each investment idea. He said that is in accordance with his system. But anyway, we, we’ve written several papers together on the Gerber statistic within modern portfolio theory and have demonstrated that you get better performance with less risk by replacing historical co variance with the Gerber statistic. And Harry and I actually, we only had really one disagreement. And the one disagreement was on factors. There’s all these, you know, factor methodologies and Harry believed that only one factor matters for portfolios. And go on, I think, I think two factors matter.

00:22:30 [Speaker Changed] So,

00:22:31 [Speaker Changed] And so that that’s but the other 23 factors, I was gonna say, we both agree are complete nonsense.

00:22:36 [Speaker Changed] So if you look at the Fama French model Sure. Which started out as yes, two or three factors, right? And then became five factors

00:22:43 [Speaker Changed] Precisely and then grow and grow. If you speak to the research departments of Bar ax, they’ll tell you that 34 to 40% of a stock price movement can be explained by factors.

00:22:57 [Speaker Changed] Okay? So it’s that a third, let’s call it

00:22:59 [Speaker Changed] A third. And of that third, 85% of that third can be explained by the first five factors.

00:23:07 [Speaker Changed] Okay? Means that, so you’re giving credit to five, which

00:23:10 [Speaker Changed] That’s bar and Axioma tells you 85% of the 40% can be explained by five factors, which means the other 20 factors explain the 15% of 40%. In other words, 6% of a stock price movement can be explained by 21 factors. Right? Meaning tiny, tiny little, which is complete, you know, nonsense but noise. If you lever a portfolio up, you know, 10 times, all of a sudden that 6% looks like it’s 60%. But it’s all complete nonsense. It’s numerical, mumble, jumbo. It’s part of the whole Wall Street pizazz that is not based on reality, but you know, it sells. So,

00:23:49 [Speaker Changed] So I want to guess the two factors. Yeah. If I had to guess, I’m gonna rely on a paper by Wes Gray of Alpha Architect and guess it’s value and momentum. But I’m curious what you found.

00:24:00 [Speaker Changed] Well actually Harry thought it was market. I think his market and sector,

00:24:04 [Speaker Changed] So is market and sector, but are those really factors? Do we really

00:24:07 [Speaker Changed] Consider this? The whole idea of factors is kind of like, you know, a little nonsense. It’s like beta, you know, like market we think of as beta, right? But right. It’s now been called a factor. So,

00:24:19 [Speaker Changed] Oh, I never really thought of beta as a factor. It’s just, it’s, hey, if you do nothing, you get

00:24:26 [Speaker Changed] Beta. Right? But that’s market. Right. You know, so,

00:24:28 [Speaker Changed] Huh. That’s really it. So you are looking at the sector it’s in and the overall market as the two driving factors.

00:24:34 [Speaker Changed] I think those are, yeah. Huh. That’s really interesting. Now it’s true that momentum value, these other things are relevant today because everyone else has glommed onto it because we have so many statistical process driven strategies that try to trade momentum, you know, buy cheap, sell expensive, it pushes everything in line. And this is what I found on the floor, using models to trade options that the models would push the values of the options into alignment in accordance with the model because everyone’s using the same model. And so the same thing is true in the broader market because everyone’s using basically the same factor models. It pushes things in alignment, which works in normal market environments, but when things, you know, have a dislocation, it no longer works, which is why people say, oh, our risk model broke down, or whatever, because these aren’t really risk models. Now it’s one thing to use a model to trade because a model’s telling you something is some expensive or cheap and

00:25:35 [Speaker Changed] Relative to history,

00:25:36 [Speaker Changed] Right? And if something’s always cheap, you just adjust the model. So there’s a validity to that. But that’s different than using the same model for risk management. Risk management again, is about avoiding unexpected loss.

00:25:48 [Speaker Changed] Huh? That, that’s, that’s really interesting. The, so when I started on a trading desk, one of the things that I was always taught, which I never contextualized as a factor, is, Hey, what’s driving the stock? Well, the stock is only a tiny part of it. The stock is 20%, the sector is 30%, and half is the market. So you could be the greatest stock in the world if the market’s going down, it doesn’t matter. And it could be a really good stock. But if it’s in a terrible sector, you know, the, the metaphor was always great house in a crappy neighborhood is a crappy house. You are really putting that into the context of these are the broader factors that are affecting that single holding.

00:26:34 [Speaker Changed] That’s right. That’s right. And, and you know, in our, at Hudson Bay, we seek to produce the alpha. So it’s true that the market is moving the stock, but we try to pick stocks that will outperform the market or pick shorts that will go down more than the market. So we seek to focus on the alpha provision.

00:26:54 [Speaker Changed] So, so let’s talk about something related to this. A paper, you published environment eats culture for lunch. It sounds like the environment is what the market’s doing, what the sector is, but give us a little detail about

00:27:08 [Speaker Changed] That piece. Well actually, I mean, that, that paper was related to the human aspect, not the market. So Peter Drucker came up with this idea that culture eats strategy for breakfast. That corporate culture is actually more important than corporate strategy for the success of a firm. I think there’s a lot to that, that, you know, the way people work together in an organization. But I’ve always thought that this corporate culture thing is nonsense. If you have people try to describe their corporate culture, they cannot articulate it. Right? You know, like, what’s the corporate culture here at Bloomberg? You know, like fun,

00:27:47 [Speaker Changed] Data driven, it’s all about data. So you come up on the,

00:27:50 [Speaker Changed] The data driven is not a culture, data driven is a process. But I’m talking about what’s the human aspect of it? What’s, what’s the human culture?

00:27:57 [Speaker Changed] I’m the wrong person to ask that because I’m

00:27:59 [Speaker Changed] Right. Because no one can really describe corporate culture, what you can describe as an environment. What is the environment that people work within? And I, I kind of learned this at Bain and Company because Bain was described as this like fun loving place. Everyone has fun. And then when I was there, two guys died in the locker bee crash. And Bill Bain had milked the esop. And so the company almost collapsed when I was there. They fired half of my class, not me. They fired all the incoming MBAs. And it was the avarice of Bill Bain that nearly collapsed the firm we’re talking back in 19 89, 90. So

00:28:38 [Speaker Changed] The corporate culture was rapacious greed. And it, it, you know, it almost destroyed

00:28:43 [Speaker Changed] That It was inauthentic. It was inauthentic. And, and when people try to describe culture, they can’t. And so what I wanted to do was to describe an environment. What is the environment that you wanna work within? And you know, when, when you speak to, when you speak to people in other firms, what’s your corporate culture? What’s your value statements? Usually these things go on and on and on. No one can really remember all the value statement. And if you can’t remember your value statement, it has no value.

00:29:12 [Speaker Changed] I’m gonna imagine that 22, 23 when all the big firms were saying, we want our employees back in the office, we don’t want any more remote work. It’s a matter of corporate culture. How did you think about that? Was this a legitimate demand and, and is it not so much corporate culture, but we want an environment where people are in the office working together. Is that legit?

00:29:38 [Speaker Changed] Well, I hate going in the office and seeing people not there. Right? I think that people should work together. On the other hand, you can’t force these things. You can’t force independent thinking. You can’t force collaboration. You can have an environment that engenders it. And so we try to have an environment that engenders it. So it’s my opinion that people who come to the office are gonna succeed more than people who don’t. Now I understand that, you know, the commute is a hassle and sometimes people, you know, want to take the day off. And so, you know, our standard is two days in the office. Many teams have a third day, but a lot of people, usually people are in our office three to five days a week. But we don’t force it. If once you force people to be in the office, I think you’re losing the esprit decor. We want people to wanna work at Hudson Bay. If they don’t wanna work at Hudson Bay, they should go elsewhere. But to force people, I think, you know, for high performers, I don’t think that’s the way to engender the right environment

00:30:42 [Speaker Changed] And environment beats culture for work because the work environment is more important than some statement that nobody remembers. Correct. So you guys have, let’s talk a little bit about independent thought. You guys have done pretty well when the experts were wrong. You thrived in oh 7, 0 8 and nine, you were notably up in years where most people were down again, in Q1 of 2020, you guys did really well. All periods of big market turmoil. I don’t know what you were doing in 2001 two, but I’m imagining the same approach held true. How do you think about these periods? Are they truly black swans or are they things that with the right approach to risk management are create opportunities?

00:31:34 [Speaker Changed] I I, again, people are trying to assess risk based upon some kind of parametric distribution with, you know, standard deviation movements. And I think that’s just nonsense. The markets don’t work like that. So our system enables us to weather all market environments through the deal code system by ignoring those parametric. The Gerber statistic, which is the basis for the work with Harry, is a rank order statistic because it recognizes the failures of parametric normal distributions. And what we do is we set a threshold because a lot of data is noise in the markets. If the s and p moves by 10 basis points, it doesn’t communicate to you how the s and p affects other things. Yet in all these statistical models, they’re including every single data point. Because if you don’t include every single data point, then in the matrix math you have a divide by zero issue. So they’re forced in all these correlation statistics, these regression analyses to include every single data point with the Gerber statistic, we are able to create thresholds where we ignore data below a certain degree of movement. Right? And so that enables us to focus on, meaning everyone wants meaningful relationships, right? Right. Of course. So this is how we’re able to focus on meaningful relationships within the market.

00:33:00 [Speaker Changed] You know, we talked a little bit about subprime real estate and how the models, it wasn’t even that they broke. They were so poorly constructed, they were destined to fail. You know, if you build a house really poorly, you don’t need an earthquake, eventually it’s just gonna collapse under its own weight. But I have to ask you some questions about real estate, because Hudson Bay has been increasingly invested in private credit and real estate. You’ve done a number of major refinancings in and around New York City, six 20 Avenue The Americas is a, tell us a little bit about the work you’re doing at Hudson Bay with private credit and real estate.

00:33:39 [Speaker Changed] Well, we saw beginning with the higher, the transitory higher rates, which we thought was nonsense, right? We saw that rates were going to be higher for longer. And we had believed that the market had been anchored in this idea of ultralow rates, which was really a manipulation of the monetary system, right? So we started thinking about what’s the implications of that? And came to the notion that the banking system would be under stress. And what’s the implication of the banking system under stress? Well, that means that they can’t extend loans in the same way, you know, corporate as well as real estate. So we started staffing up in those areas to take advantage. And, and now I’m convinced that the, there’s now going to be a structural shift in credit provision in the US economy that the banks are no longer going to be the mainstay for credit. And that’s because the government has effectively guaranteed our banking system, which creates moral hazard. We have on the order of, you know, 4,300 banks in the United States. It’s a lot, especially when you compare it to Canada that’s got the big, you know, handful. And you know, when you deposit money in the bank, that bank is lending it out long

00:35:03 [Speaker Changed] And, and fractionally reserving it. So it’s 10 to one, 20 to one, whatever the precisely the leverage they’re using.

00:35:10 [Speaker Changed] So I think that the whole fractional banking system notion is challenged, particularly in the idea of the ease of information transparency among depositors, coupled with the necessity for government guarantee and moral hazard. So private credit firms like ours, people invest in Hudson Bay and they know it’s not a bank account and that gives us license to deploy the money in ways that are appropriate. And so we began staffing up in those areas. And now in real estate, for instance, we have teams that work in real estate equity in CMBS distress, CMBS and direct provision of real estate credit. And as part of the core value of Hudson Bay, these teams work together, which give us a better understanding. It’s a great advantage to have equity teams working with credit teams, particularly all real estate’s local. It gives us a much better understanding of the asset that we’re looking at. Huh.

00:36:16 [Speaker Changed] That, that’s really kinda interesting. You know, ever since the financial crisis, some of the new regulations and bank regulations directly led to the rise of private equity, private credit, you know, some of the forecasts are over the next decade. This blows up to a $13 trillion asset class.

00:36:37 [Speaker Changed] I think we’re in the third inning now.

00:36:39 [Speaker Changed] Ear early days

00:36:40 [Speaker Changed] Here.

00:36:40 [Speaker Changed] Yeah, I think so. And, and it, it feels like it’s been so big. ’cause you, we started with practically nothing in that space and the first couple of trillion dollars felt like, oh my goodness, there’s just so much capital washing over this. But this seems to have happened in the past where Wall Street banks and brokers kind of move up market, they create a void in the space they left and private money rushes into fill that void. Is that what’s going on with private credit and real estate?

00:37:14 [Speaker Changed] Well, it’s still early in that I think it’s a golden age for real estate credit. The banks are not able to, they don’t have the capital now to lend. And so there’s, it’s, it’s open season. Huh,

00:37:27 [Speaker Changed] Really, really interesting. So how do you identify opportunities in the real estate space? It seems like there are so many buildings that are half empty and yet it’s a slow motion train wreck because most of their tenants have 10 or longer year leases and they’re just slowly starting to recognize, unless you’re a super a class building, even a buildings are having a hard time attracting renewals and tenants. How do you identify these and how far along the repricing of commercial real estate or at least offices do you think we are?

00:38:09 [Speaker Changed] Well, those are big questions and I’m from Ann Arbor, Michigan, and I saw how in Detroit, Detroit was gonna be called the museum to the, I dunno, desolate city because downtown Detroit went empty when they built the Renaissance Center. Everyone moved to the Renaissance Center and left these empty huge buildings in Detroit. And you see aspects of that now where the, the a buildings, the new buildings are attracting very high rents and buildings in other areas are, you know, going empty. So to understand what’s going on, you really have to understand the asset. And so that’s why it’s important to have teams from different disciplines being able to understand the asset, obviously looking through the rent rolls and understanding, you know, the weighted average lease, but also understanding the macro environment, you know, are things growing and, and we have so much uncertainty now going on, not just because of work from home with Zoom, but also the longer term implications of AI and what’s that gonna mean for the workforce. And even cities like New York City, it’s possible that we’re not gonna need the same number of junior lawyers, junior accountants, junior bankers.

00:39:26 [Speaker Changed] So I’ve heard some people discuss AI as a tool, and it’s not that you’re gonna lose your job to ai, but you’re more likely to lose your job to someone working with ai. Is that a fair assessment or is it just still way too early to

00:39:42 [Speaker Changed] Tell? I think we still don’t know. I think AI is the greatest change in my lifetime.

00:39:47 [Speaker Changed] Bigger than the internet?

00:39:48 [Speaker Changed] I think so, yeah. Really? Yeah, because the ability for natural language processing goes far beyond what I thought was possible. You know, I studied linguistics a bit in college and the whole idea of how we form language is a fascinating subject. And now the computer is able to be cogent in their responses. It’s, it we’ve, you know, kind of approaching hard AI in a way that I did not think was, was possible and it’s only gonna get better.

00:40:18 [Speaker Changed] Let let me push back a little bit, and I’m not necessarily saying I believe this, but, so I’ve, I’ve had this conversation over and over again with a number of different people. How are you using AI in your daily work? What, what are you finding? And someone who ho hosts a different podcast said, they created this really interesting set of prompts with AI to get an answer to how to do certain things. And the first time they got the answer, they were really impressed, oh my God, this is a genius insight and look how smart this is and how it, it figured out exactly what I needed. And then they asked a different question with a different subject, kind of got the same answer and it was like, oh, this is a party trick. This isn’t really intelligence, it just looks like intelligence. And even though it’s getting better, it’s still kind of dumb relative to it impresses us. But once you peer behind the curtain and see the wizard is Yeah, just a man you figure out, yeah. Oh, this is less what it purports to be in more like a very useful, clever trick.

00:41:38 [Speaker Changed] Yeah, I I was thinking of the Wizard of Oz also while you were, while you were saying that, but I don’t think there’s a guy behind the curtain that’s giving the answers. That’s why I think that it helps with the junior analyst that you have to check anyway. And it, it certainly speeds up the research process in ways that were not possible before for sure. And it’s only gonna get better and it makes mistakes. But the junior analyst makes mistakes also. I mean, I’ve used it for things, my, my lawyers probably will hate me, but sometimes when I’ve had a discussion with the lawyers on how to express something in a document, I’ll ask AI the question, it’ll gimme a range of possibilities and enables me then to be more on a level playing field with my lawyers who’ve had a lot more experience than I have. But it has enabled me to bring to the discussion insights that we might not have thought of.

00:42:28 [Speaker Changed] I’m gra glad you brought up the attorneys because a judge just sanctioned a lawyer for using AI and to in certain of its answers. Yeah. And this unfortunate tendency to hallucinate, right? He, he, I don’t think the problem was that he used AI to help him in research. Right. He didn’t double check it. Right. And he failed to disclose that AI was part of the process.

00:42:52 [Speaker Changed] It’s, you know, yeah. It’s just plain laziness. The, the a the AI is good for the junior, you know, person. Right. And I think that has implications for the workforce. You know, what is the workforce going to look like given that maybe we don’t need the, the same phalanx of junior accountants, junior lawyers, junior bankers,

00:43:12 [Speaker Changed] How do you become a senior account lawyer banker if you’re never a junior? It’s a, it’s a tough question. So let me give you an opportunity to update your 2021 piece in investing. Don’t short human judgment. Right. Do you, are you still holding that for

00:43:29 [Speaker Changed] You? Absolutely. I mean, we are in the human judgment business

00:43:33 [Speaker Changed] Really.

00:43:34 [Speaker Changed] We, we are trying to beat the machines. We do that, as I said, through understanding uncertainty, events catalysts and change. And I think ultimately human judgment is superior in the machines. I hope we won’t go into a Hal 2000 type situation. That human judgment will always be superior. You wouldn’t want to have a machine be the president of the United States. How could a machine possibly make those decisions? You know? So obviously human judgment will always be there. And I don’t think that we’re at a terminator type, you know, situation. But there are certain experts that say that ultimately that’s where we’ll go. I mean, I do know that in the military, you know, the idea of robots creating robots is a real idea and it very might well change battlefield dynamics. But I believe that certainly at this point in time, the human capacity to ingest a mosaic of information and to make the right decision is superior.

00:44:42 If you take, if you take a chess board, the machine can beat the master, but if you put an extra bishop on the board, the machine can’t deal with it. Right. And I think that’s the paradigm. And life does not mimic a chess board, you know, life mimics the chess board with extra pieces being put on randomly. And is that randomness that I don’t think the machines will be superior than human judgment. Now it might appear at times that the machine can beat the human, but I think ultimately the human judgment is superior. And so our business is based on human judgment.

00:45:18 [Speaker Changed] You mentioned the wartime usage of ai. There was a pretty big article, I don’t remember, I wanna say the times, not the journal that figured out that in the Ukraine Russian War, which started out as a conventional bombardment between tank tanks and mortars and anti-tank weapons, over the past six, 12 months, 70% of the casualties have been drone AI warfare driven. And it’s very much a brave new world. It’s not like the old world of warfare. What it sounds like you’re suggesting with AI is that they’re both gonna co-develop that you’ll still have humans driving the process, but AI is gonna become an increasingly large part of it, regardless of whether we’re talking about warfare, business or investing. I don’t wanna put words into your mouth, but is that a fair way to assess that?

00:46:15 [Speaker Changed] I think so. I mean, I think that the humans always have to be on top of the machines. Machines have a lot of latitude both to produce themselves is as well as to target. You know, the markets are different because the markets follow a behavioral dynamic. The valuation of risk versus

00:46:33 [Speaker Changed] Reward

00:46:34 [Speaker Changed] Is something that I think a machine cannot do in the same way that human can. So

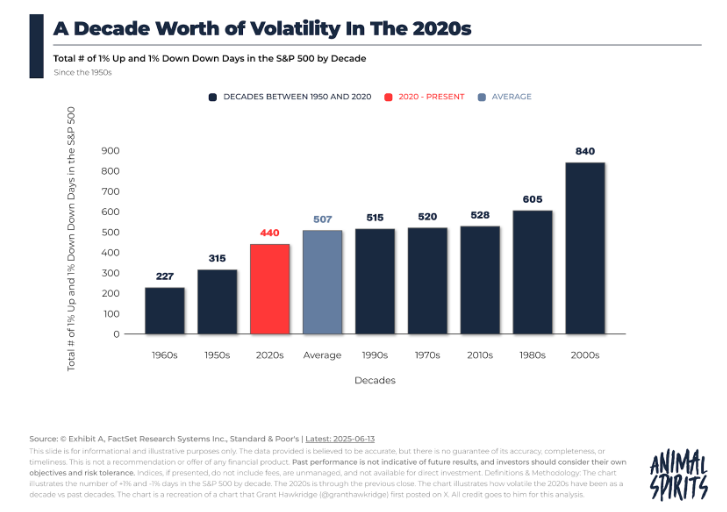

00:46:39 [Speaker Changed] Given some of the volatility we’ve been seeing in the first quarter of 2025, has that changed how you’re looking at your models, how you’re viewing your approach? Or is it, hey, this is just another one of those things that comes along and we have to be able to trade through it.

00:47:00 [Speaker Changed] We actually like the dislocation because the dislocation proves the models are wrong.

00:47:06 [Speaker Changed] I know you guys don’t release public performance numbers, but I know you are doing much better than your benchmark this quarter. Volatility is your friend, is that what you’re saying? Yes. Because volatility disrupts traditional models and you’re a non-traditional model. Correct. So I know you’ve worked with Harry Markowitz. What other academics and what other institutions have you worked with?

00:47:29 [Speaker Changed] Well, at Imperial College London, there’s further work being done on the Gerber statistic and incorporating it. The idea of thresholding data and ways to do it to, for instance, if you want to understand the significance of a stock price movement, maybe should exclude days where there’s very low volume and only include days when there’s high volume. But there’s a variety of ways to incorporate it.

00:47:57 [Speaker Changed] I know I only have you for a limited amount of time. Let me jump some of my favorite questions. I ask all of our guests, what are you watching or listening to? What, what’s keeping you entertained?

00:48:08 [Speaker Changed] Recently? I streamed Eastern Gate.

00:48:10 [Speaker Changed] Oh

00:48:10 [Speaker Changed] Really? Which is I saw in the New York Times. It was this spy thriller series on the conflict between Poland and Belarus. And I wanted to understand the dynamic between it. So I thought I’d get a little entertainment and understand something I couldn’t pick up here. And it’s a little slapstick, but I think it’s worth it.

00:48:30 [Speaker Changed] Eastern Gate. Yes. Did you happen to watch any of fada when that was Yeah, I

00:48:35 [Speaker Changed] Watched all of

00:48:35 [Speaker Changed] Fada. Just most heart wrenching stuff to watch. Yeah, it’s so stressful.

00:48:39 [Speaker Changed] Yeah. And pretty realistic, I think.

00:48:42 [Speaker Changed] Very realistic. Let’s talk about mentors who helped shape your career.

00:48:47 [Speaker Changed] I gotta give a lot of credit to Dave Petraeus,

00:48:50 [Speaker Changed] Who I know that name,

00:48:52 [Speaker Changed] Who really helped me get into shape. And he was on my case every day, the diet, the working out, we were workout partners and I was 35, 40 pounds heavier. And he got me to recognize they needed to get in shape. I thought I was in shape, but I wasn’t in shape. I think, I think a lot of people think they’re doing okay when they could do a lot better. Right. And he taught me I could do a lot better. And I think it’s affected me overall. My mental acuity, my mood, my, my stamina. I really give ’em a lot of credit.

00:49:30 [Speaker Changed] You mentioned books earlier. What are some of your favorites? What are you reading right now?

00:49:33 [Speaker Changed] One book that I really enjoyed, which was long, was Walter Isaacson’s book on Elon Musk, which I, I read before the election. Right. And it made a big impact on me because I believe in questioning the experts, but Musk takes it to a different level. He’s questioning metallurgical properties that were well grounded in science and engineering. And he’s saying, why does that have to be? And oftentimes he was right that the established consensus regarding properties of metals was wrong.

00:50:04 [Speaker Changed] Hmm. Really, really interesting. Any other books you wanna mention?

00:50:09 [Speaker Changed] I read The Melting Point by Frank McKenzie recently. He was the head of centcom and he talked about what it was like to lead centcom and he also had a ma, he majored in English and he thought that his English background to be a commanding general, it was very helpful because I helped him to articulate better and to form consensus, you know, among his colleagues.

00:50:36 [Speaker Changed] Hmm. Really, really interesting. Our final two questions. What sort of advice would you give to a recent grad interested in a career in either fill in the blank, investing options, trading, multi-strategy management? What advice would you give to

00:50:54 [Speaker Changed] Them? Well, I think it’s, you know, across all certainly service occupations is you gotta be able to beat the machines. And to do that, you need to be independent thinker. You need to go against the grain question, the experts. You need to be able to, to do that, you need to work with other people to learn from them, to expand your horizons, to expand the mosaic that you can bring to your independent thinking. And you gotta be able to respect your colleague. So I, I think that those three things are, are real guideposts for

00:51:28 [Speaker Changed] People. This goes back to your corporate culture, which is

00:51:31 [Speaker Changed] Corporate environment.

00:51:32 [Speaker Changed] Corporate environment. My bad. Your corporate environment. Think independently, collaborate and respect the individual. Correct. Huh. And our final question, what do you know about the world of investing in finance today would’ve been useful when you were first getting started in the early nineties?

00:51:51 [Speaker Changed] I think that, you know, everything you learn in business school or economics, you can just throw out the window. Economics is not a science. People try to portray economics as a science, and it, it simply is not. And so all the notions that we brought up regarding money supply, you know, Milton Friedman would be turning over in his grave even though these principles might have some grounding. It’s not scientific, you know, this is, this is not a natural science. It’s a behavioral science and it’s based upon how people interact with each other. And I think that that appreciation leads to the notion that oftentimes the academy or the experts try to proffer things that everyone, everyone seems to believe one way. And you think, how could I be right? Because everyone believes one way because this is what they studied in school. And the authorities say it’s that one way. And I think that as you go through life and you age, you realize that the ivory tower isn’t always correct. In fact, a lot of times the ivory tower doesn’t have the real life experience and so they’re flat out wrong.

00:53:03 [Speaker Changed] I’m trying to remember where, where I’m stealing this quote from. Science advances one funeral at a time. The same is true with other things. Dick Thaler said, rather than wait for the rest of economics to catch up with behavioral finance, I’m just gonna teach it to the younger generation and it’ll, it’ll infiltrate much more quickly than waiting for all of my peers to, to accept it. Really, really fascinating. Sandra, thank you for being so generous with your time. We have been speaking with Sandra Gerber. He is CEO and CIO of Hudson Bay Capital. If you enjoy this conversation, well be sure and check out any of the previous 550 we’ve done over the past 11 years. You can find those at iTunes, Spotify, YouTube, Bloomberg, wherever you find your favorite podcast. And be sure and check out my new book, how Not to Invest the ideas, numbers, and behavior that destroys Wealth Out today. Wherever you find your favorite books, I would be remiss if I did not thank the correct team that helps with these conversations together each week. John Wasserman is my audio engineer. Anna Luke is my producer. Sean Russo is my researcher. I’m Barry Riol. You’ve been listening to Masters in Business on Bloomberg Radio.

The post Transcript: Sander Gerber, CEO and CIO Hudson Bay Capital appeared first on The Big Picture.