Nvidia (NVDA) Bull, Base, & Bear Price Prediction and Forecast (April 2)

AI darling Nvidia is at a crossroads, and many are confused about where the stock could go next. Here is a bullish, base, and bearish analysis of where shares could be in 2030. The post Nvidia (NVDA) Bull, Base, & Bear Price Prediction and Forecast (April 2) appeared first on 24/7 Wall St..

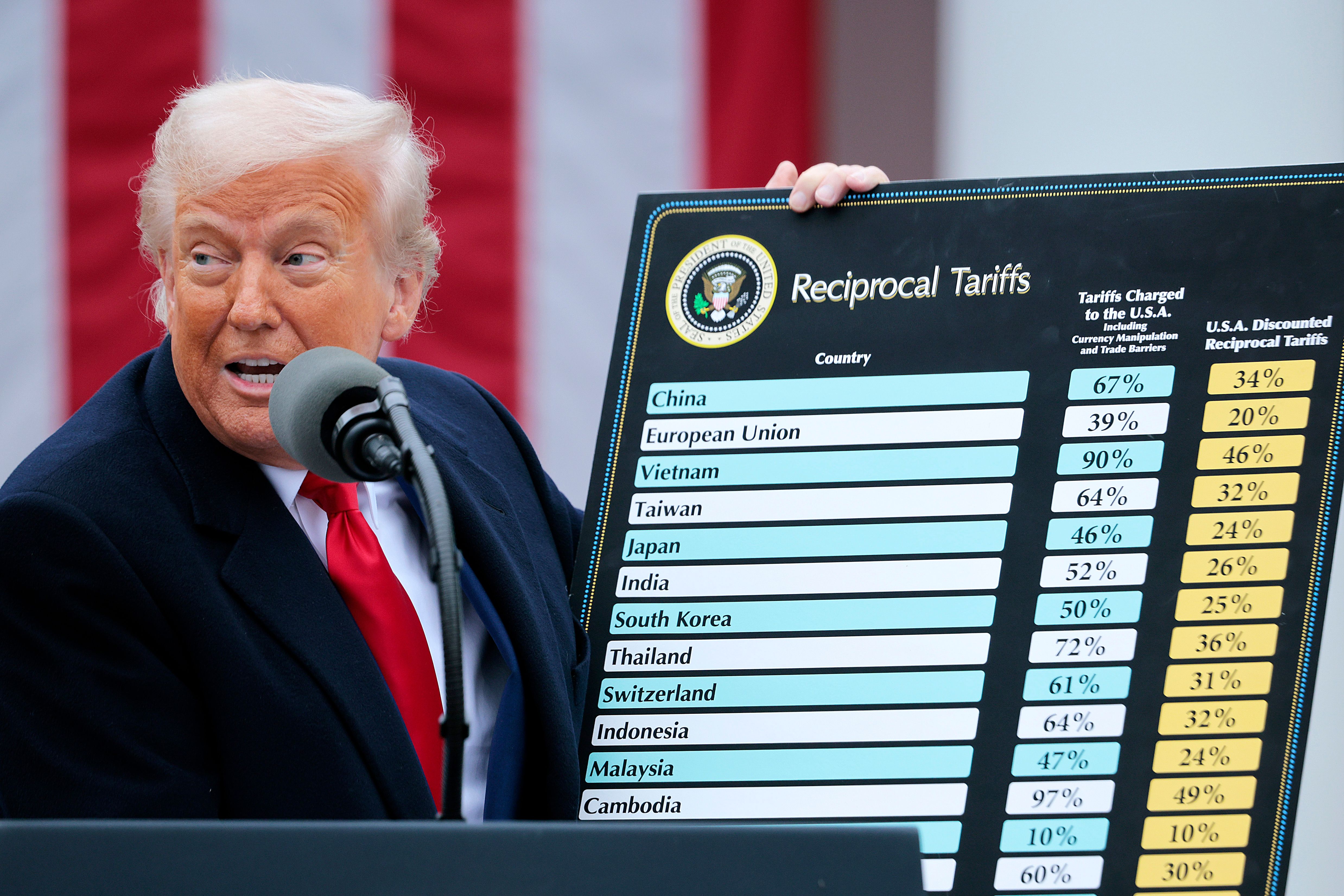

Nvidia Corp. (NASDAQ: NVDA) shares are trading near a year-to-date low. Like its fellow Magnificent 7 members, Nvidia has struggled due to economic uncertainties due to the potential effects of tariffs, as well as to Chinese AI innovations. Bears see Nvidia stock falling further due to bearish pressure from the broader market. Yet, some investors remain optimistic for a sustained rebound in the coming months. Perhaps even a revisit to all-time highs if tariff fears dissipate and macro data gets better.

24/7 Wall St. Key Points:

-

Nvidia Corp. (NASDAQ: NVDA) stock has fallen to a year-to-date low.

-

The AI darling is still at a crossroads, and many are confused about where the stock could go next.

-

This analysis looks at three scenarios and where Nvidia stock could be in 2030.

-

Nvidia made early investors rich, but there is a new class of “The Next Nvidia Stocks” that could be even better. Click here to learn more.

The bearish argument has won out on Wall Street so far this year. While the AI rally can return if things improve, it remains speculative, whereas the reasons for Nvidia stock’s decline are genuine.

Nvidia is at a true crossroads right now. We do not know for sure where the stock will go next, but with the data on hand, we can speculate. That’s what we are doing here.

Three Key Drivers of Nvidia Stock Performance Through 2030

1. AI Infrastructure Dominance: Nvidia controls an estimated 80% of the AI accelerator market through its H100/H200 GPUs and CUDA software ecosystem. It is tough for Nvidia customers to switch to another supplier, and this has allowed it to dominate the industry, with customers coming for more year after year. As such, it is well-positioned to capture growth from the $400 billion AI chip market projected for 2030.

2. Data Center Expansion: Its data center revenue has surged from $4.3 billion in Q1 2023 to over $35.6 billion in Q4 2024. Maintaining leadership here requires continuous innovation in GPU architecture and energy efficiency as AI workloads grow exponentially. So far, Nvidia has managed to do that.

3. Margin Preservation: One of the biggest arguments against Nvidia is that it may not be able to hold on to its massive margins as competitors catch up and become more attractive to Nvidia’s customers. This has yet to happen, and Nvidia has been able to defend its hold on the market quite well. In turn, this has allowed the company to have industry-leading gross margins at 73% in Q4 FY2025.

Nvidia Stock Price Prediction in 2030: Bull, Bear, & Baseline

24/7 Wall St. estimates that Nvidia’s stock price in 2030 will be $491 per share in our bull case, $362 in our base case, and $38 in our bear case. Each of these estimates comes from a specific scenario analysis of Nvidia’s business segments.

Bull Case for Nvidia’s Share Price

Assumptions for our bull case are as follows:

- AI growth: Nvidia currently holds about 80% of the AI accelerator market. Analysts project this dominance could continue through Blackwell GPU adoption and CUDA’s software moat. This may allow data center revenue to grow at a 25% CAGR to $351 billion by 2030 vs. $115.2 billion in FY2025. Gross margins could remain above 70% due to limited competition in high-end AI training chips.

- Automotive & robotics: A 50% CAGR in automotive revenue to $25 billion by 2030 is achievable if Level 4 autonomy reaches even 15-20% penetration.

- Software: CUDA is already a big part of Nvidia’s moat, but this could get even better if the AI narrative succeeds in the long run. Perhaps Nvidia could even shift this to a SaaS model once more developers become dependent on it.

All things considered, $491 per share is possible with around $240 billion in net income if all that revenue materializes and margins hold up. Investors will still have to pay a 50x TTM earnings multiple for the stock. The market cap would be $12 trillion.

The likelihood of this happening is quite low due to the amount of ground Nvidia would have to cover.

Base Case for Nvidia’s Share Price

Assumptions for our base case are as follows:

- AI growth: Data center growth can grow at 15% CAGR to $230+ billion by 2030. If Nvidia retains a 60% to 65% market share here, it could reach that goal, especially if competitors keep falling behind.

- AI narrative success: The AI narrative would still have to succeed for Nvidia to reach our base case price of $362. Otherwise, there would be no growth, and investors would quickly slash the growth premium to a discount.

Nvidia’s valuation for the base case would be $8.9 trillion. I strongly recommend reading this share price forecast for a more detailed analysis of our base case.

Bear Case for Nvidia’s Share Price

You may have noticed that there is a big gap between the base case and the bear case, and this is mostly because the bear case assumes that the AI narrative would fail.

If that happens, the result would be catastrophic for Nvidia and its stock. The only reason the shares trade at such a high valuation is that it is directly linked to AI and its prospects. Without it, it will return to being known as a gaming GPU company with some links to crypto mining.

Obviously, that will not happen. AI demand is not going to disappear overnight. However, what can happen is that AI development could slow down. As a result, Nvidia would slow down too. It needs continuous orders from hyperscalers and AI startups to maintain its momentum and strong margins. If AI slows down and companies are no longer willing to run massive AI models at a loss, they’re also unlikely to upgrade their GPUs to whatever Nvidia has to offer. This would crush Nvidia’s margins and turn revenue growth red, and investors would no longer pay a growth premium for the stock. $38 for such a scenario is reasonable, if not a bit rich, considering that would still leave Nvidia with a $932 billion valuation.

Regardless, our baseline remains at $362 for 2030.

The post Nvidia (NVDA) Bull, Base, & Bear Price Prediction and Forecast (April 2) appeared first on 24/7 Wall St..