NRG CEO Larry Coben rides the power wave with big deals as the S&P 500’s biggest riser in 2025

NRG is doubling its natural gas-fired power plant fleet through acquisitions and preparing to thrive with or without the data center power boom.

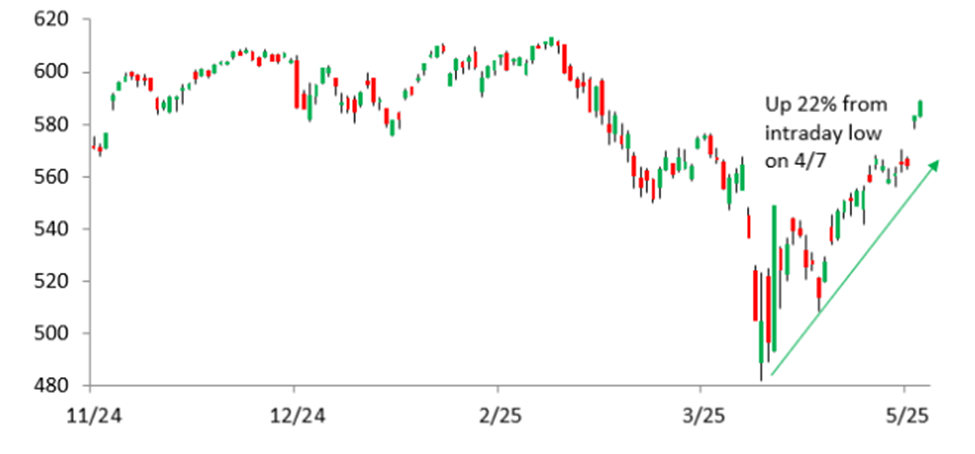

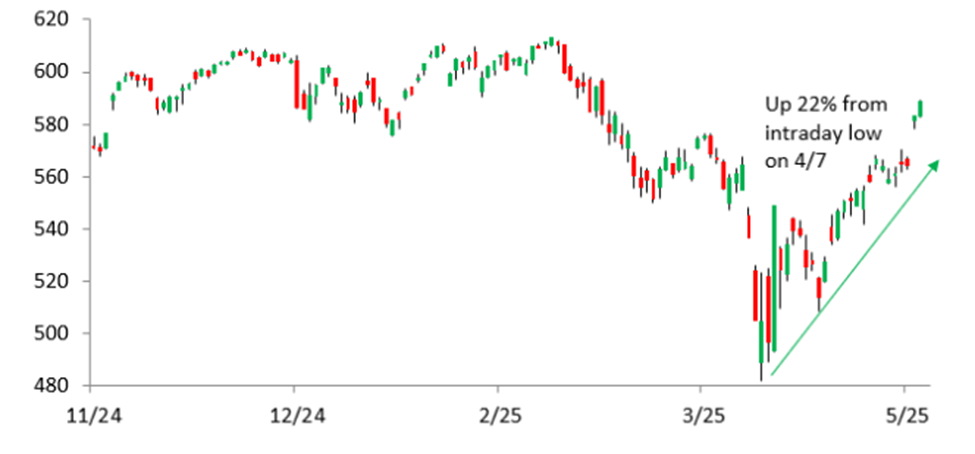

HOUSTON—Move over, Palantir and Uber. The S&P 500’s top-performing, large cap stock in 2025 is the redundantly named NRG Energy.

A growing power generator and retail electric business, NRG’s energized stock has surged by 75% this year, and by about 240% since chairman Larry Coben also took over as interim president and CEO in November 2023 amid an activist push from billionaire Paul Singer’s Elliott Investment Management.

An NRG board director since 2003, Coben, an energy entrepreneur, archaeologist, and philanthropist—yes, that’s a confusing mouthful—is now leading NRG with regular Wall Street beats and big acquisitions after years of stock market underperformance.

Earlier in May, NRG—ranked 150 in the Fortune 500—agreed to pay nearly $10 billion for 18 natural gas-fired power plants from LS Power in a move designed to prepare NRG for a domestic power market that’s set to soar. The acquisition essentially doubles NRG’s gas-fired power generation to help fuel the oncoming data center construction boom and to better balance intermittent renewables on grids.

A decade ago, after a previous NRG CEO was ousted for pivoting too quickly to green energy, Elliott first entered the picture to sell off NRG’s renewable assets—now Clearway Energy.

After NRG paid $2.8 billion to buy Vivint Smart Home in 2023, Elliott again jumped in to successfully remove Coben’s predecessor and to emphasize a focus on NRG’s core business. Coben took the role on an interim basis not realizing he’d end up happily stuck with the job.

With power set to explode in the U.S., Coben tells Fortune NRG is primed to thrive even if the data center boom never takes off.

The following has been condensed and lightly edited for clarity.

I realized that NRG is the top-performing S&P 500 stock of the year. Obviously, you’ve exceeded expectations of late with income, Ebitda, cash flow, and other metrics. What stands out to you and why is NRG beating a lot of targets?

I think we’ve been a company of incredible potential and, since I’ve been here, we focused on a few things. One is really a laser focus on operating performance, which is the only thing that lets you do the other things that we’ve been doing in terms of growth and acquisitions. If you look at the last quarter that got a little bit lost in the acquisition news, we got a big beat. We beat consensus by a couple hundred million bucks, and it was across every sector of the business. We probably never performed this well in generation, in retail energy, or in smart home. I think you’re just seeing that super focus in our core business, making us better and better every quarter. We’re only still scratching the surface of what we’re capable of.

“When you’ve been in a world where there’s been no [U.S. power] growth for 20-plus years, soaring is 2% to 3%. Some of the [bigger] numbers that are out there, even we don’t believe. We tend to talk investors down sometimes.”Larry Coben, CEO, NRG

You’re making a big bet on soaring domestic energy demand, including data centers. How is that going to play out and what’s NRG’s role?

Soaring has a lot of meaning, so let me drill down if I can. There are all kinds of numbers out there. When you’ve been in a world where there’s been no [U.S. power] growth for 20-plus years, soaring is 2% to 3%. Some of the [bigger] numbers that are out there, even we don’t believe. We tend to talk investors down sometimes. Two to 3% would be enormous when you think about the amount of capital needed to get this done. So, it’s a bet, but it’s a bet that we’ve made very conservatively by buying it in a very attractive price. It’s right in our lane. This is what we’ve been doing every day for a very, very, very long time.

Our assumptions are pretty conservative, and yet we’re still looking at 40% higher earnings per share per annum growth on a compound basis. If we get soaring demand growth, that would be even better, but we don’t need soaring demand growth. We’re betting on a normal tightening of the market, but we didn’t even put tightening of the market in the numbers to get the 40% growth, just to be super clear.

I do believe that this is a demand super cycle. I get that from talking to our customers. We have the second-largest C&I (commercial and industrial) electricity book; we’re the largest residential provider in Texas; we are the largest C&I provider of natural gas. So, we have customers we talk to every day about what they’re using and what they need. We base our thoughts on demand and what really drove this acquisition was their needs.

You just talked about being conservative, but I’ll still play devil’s advocate a little bit. What if the so-called data center boom underwhelms, whether it’s from AI becoming much more energy efficient more quickly, or from just AI utilization rolling out more slowly than anticipated?

When you look at our numbers that we projected, we have put in zero for data centers. I don’t believe that’s what’s going to happen, but we’re showing compound growth per annum on an EPS (earnings per share) basis going from 10% to 14% with no data centers or other significant large load additions. I believe data centers are real, but they’re going to be on top of all the growth that we’re achieving in our core business. I think that’s really important. I’m a big believer, and we have a great data center strategy, and I think it will drive markets and tightening even further. But we don’t need it to achieve the kind of growth that we’re talking about.

Could you elaborate a bit on that data center strategy and how you see it playing out in terms of growth?

Data centers are going to be integral to U.S. economic growth, and we need to be there to power the economic growth. We already serve most of the people who are building these data centers, the hyperscalers in our C&I business. But there’s a few ways we can serve them. If you have a data center, we can sell you power for a long-term period. With this new acquisition, we have a lot more flexibility to create products for data centers that they want longer term. How much price risk do you want? Second, we have a series of sites, 21 that we have now, and another 15 that will come with the new acquisition, that have the potential either for new power plants, or new data centers, or some colocation combination of the two.

The third leg of our stool is additionality. There’s a lot of concern the data centers are going to take power off the grid. We have an agreement with GE Vernova and Kiewit for over 5 gigawatts of turbines and construction, of which we already have reserve slots for 2.4 gigs. In the new acquisition, we’ve already identified another gigawatt of possible upgrades of [smaller] peakers (gas-fired peaker power plants) to [larger] CCGTs (combined-cycle gas turbine plants). We think we have that great three-legged stool to really provide a great menu for the data center builders and users of the world.

Homing in on the LS deal more, why is it so important right now to scale up, especially in gas-fired power generation?

I think this is probably the last big fleet that was available, certainly in the competitive markets where we want to be, in particular PJM (regional transmission organization in the Midwest and Northeast) and Texas. We think those are the two most attractive markets in the country. We’re doubling our generation fleet, we’re modernizing it because the LS fleet is younger than ours, and we’re acquiring it at roughly 50% of what it would cost to build it new. Then you talk about all the upside opportunities that I mentioned with tightening prices, upgrading of the new capacity on those CCGTs. It’s very exciting. Interestingly also, it enhances our credit profiles. Rating agencies are a lot more comfortable when you have iron. The last thing is, and not to bury the lead, it was a super accretive transaction.

Did you have LS in mind for a while? How did it play out over time?

We talk to everybody all the time. Aa lot of these plants are in funds that are long lived. As you know, private equity funds have finishing days. Yes, they can extend them, but I think LS Power was looking to return capital to their investors but also have some way of playing in future benefits and growth. They all looked at IPOs, but the IPO market has been super volatile. This is a way for them to have their cake and eat it too. They’re very, very happy. We had a lot of discussions about the power of the combination, and it really fits like a glove in Texas and PJM. They will own 11% of us, which will be their largest equity investment. Eventually, we said, “We need to do this,” and we did.

Please touch on the importance of LS’ CPower component of the deal and maybe explain how the virtual power plants (VPP) work and factor into NRG?

CPower is the leading demand-response platform in the country. Demand response is really the ability to get people to turn down or turn off their power usage at peak times, rather than having to generate additional power. You’re paying them, obviously, to do that. It can be more economical to pay someone to shut down than it can be to build an extra power plant and then have to turn it on, especially if you’re talking about a limited number of hours a year. It’s kind of the same function as a peaker plant. You’re going to only get to run it a few percentage points of the number of hours in a year, but it can be super important in those times of crisis where maybe it’s 115 degrees or its 0 degrees. It’s a small part of the economics of the deal today, but, as markets tighten, we view it as something that will be more and more valuable. We have our own C&I demand-response business but, frankly, we think theirs is a better platform, and we look forward to working synergistically with them on that.

Here in Texas, we just rolled out a residential virtual power plant, which will do the same thing by people agreeing to let us work with their thermostats for short periods of time in their home, which will also be a significant help for Texas in times of particular heat and cold or other high-peak use.

Switching gears a little bit, obviously, natural gas is going to be by far the largest part of the generation portfolio. Right now, it’s closer to equal between gas and coal. What’s your take on the coal portfolio and the future of coal for NRG and maybe for the coal industry as a whole?

Coal plants are still very, very economical. and more so in a tightening market. We’re not going to build any new coal plants. I don’t know if anyone is, and I don’t know of any of that are planned. It’s also grid stability. If we shut down those plants tomorrow, there would not be enough power in Texas. It would be both grid instability and inadequate capacity. Those are two really bad things. They’re an integral part of the system, and I think they’ll remain so for the foreseeable part of the future. But I don’t see us in any way, shape, or form expanding in coal. You’re correct that our percentage of gas will be 75% to 85% [after the LS deal], depending on how you want them measure. That’s a very comfortable place to be. We can’t build a grid without gas-fired capacity today. Whatever your political persuasion is—and I did my first solar deal in 1983, so I’ve seen all the cycles—until we have some long-duration affordable storage, you can’t have an all-renewable grid even if you want one. I try to speak the truth.

Why are Texas and PJM the spots you want to continue to grow and focus?

They’re competitive markets where being a well-run company with some of the most amazing people in the industry actually makes a difference. In a regulated market, you offer one product. This is what the product is, this is what the price is, and everybody’s a taker. And we can’t compete. The ability for us to offer customized, tailored solutions of various durations to all of our customers, that’s possible in PJM and Texas, in particular. That’s why we want to be there. I’m a big believer in competitive markets, I always have been, and those are the two best competitive markets by far in the United States.

Could you discuss the smaller Rockland Capital deal (Texas gas-fired power plants acquired for $560 million in March) and, longer-term, the brownfield construction projects over the next few years (new plants built in part through loans with the Texas Energy Fund)?

We have a lot of customers in Texas. We’re the biggest retail provider here and a lot of C&I. Both the Rockland deals and the TEF (Texas Energy Fund) projects are similar strategically to what we did with LS. LS is just bigger. Rockland and those TEM projects are 2 gigs. The amount of power for those in Texas is about the same as the amount of Texas power we got in LS. Adding those 4 gigs total in Texas gives us tremendous flexibility with our generation, and it enables us—if we want—to supply our entire retail load from our own generation, which we could not do before. It gives us more and more optionality in competitive markets, which we love. All of that generation is very flexible. When there’s cheap solar and wind, we’re happy to turn off our gas plants, buy that, and resell it to our customers, instead of running our plants. The TEF program is really designed to bring more gas—non-intermittent power—online. We think it’s a great program. We have those three projects in there, and we anticipate all of them will get to close and get built.

What about the integrated generation and electric strategy? How is the home retail business going with your Reliant, Green Mountain, Direct Energy, and other brands?

We’ve been doing super well, partly because one of the things we’ve been working on is integrating our Vivint smart home business with those brands. The residential VPP I talked about is the best example, but we’ve rolled out a product called Home Essentials. If you sign up for Reliant for a certain period of time, we’ll actually give you a Vivint [security] camera and [smart] thermostat. They’re upgrading their smart home systems, so we’re expanding our horizontal share of people’s wallets.

We’re really trying to make everything energy in your home easier rather than what I would say we were doing five years ago, which is sell you electricity. There’s a big difference between selling you something you actually want and are happy to have rather than, “OK, my lights went on.” It’s a strategic rollout, first in Texas and then in other parts of the world. Unlike most companies in our space, we start with the customer and work backwards. I don’t care if you’re a homeowner or you’re a hyperscaler, we want to serve you in the most optimal way possible.

I’m going back in time a little bit, and word this probably a little poorly. So that’s my fun setup. You mentioned the success of Vivint, but it was the acquisition of Vivint in part that drew Elliot back in and led to the ouster of your predecessor, Mauricio Gutierrez, and put you in the CEO role. Could you take me through that evolution from then to now?

I think Vivint is a great company and was a very good acquisition. I think it took people a while to figure that out. We could spend hours over a drink talking about why it is, but people didn’t understand it and how we got it strategically. It was also part of a big pivot of ours towards being customer centric. And you don’t hear any more about what a terrible acquisition Vivint is. People look at the growth numbers and go, “Wow, what a great deal.” The public market sometimes wants to judge everything in a month rather than taking the time to learn it. If you look at any of the stats or growth, Vivint is killing it. And, so, Elliott made a lot of money. They are [now] out of the stock, but they made a lot of money. They were out a little bit before the [LS] acquisition, but I think they would tell you they were happy shareholders. They have a way of doing business and they make a ton of money doing it. So, I can’t really argue with them. What we have done by putting our focus on operations, by creating all of these new products, by integrating Vivint in our retail business, we’ve created a powerful platform to serve everyone.

You’ve been on the board since 2003 but, when you took over the interim CEO role, the initial expectation was eventually for an external hire.

That was certainly mine (laughing).

Obviously, things have gone well since you took over. I wanted to get your take on why you ended up in the position more permanently.

You remember The Godfather Part III, when he says, [“Just when I thought I was out, they pull me back in.”]. I was trying to get out, but they sucked me back in. Look, I think we started to create a real momentum of success here. There were some cultural changes. I talked about going on offense instead of defense here because, when you have an activist, it’s too easy to kind of go into a shell because you think they’re going to attack whatever you do. We started making progress and the board, after going through its process, came back to me and said, “We’d like you to finish what you started here if you’re willing to do that.” And here I am. My only goal for 2023 was to go on Medicare. I succeeded, but then I ended up with this job too. But I’m thrilled to be here and, obviously, if I didn’t love what we were doing and love the potential that we have and didn’t want to finish that journey, I would have said no. And it’s now 18 months later, and here I am.

The other thing I wanted to ask about the past is because you’ve been on the board since 2003. Prior to Gutierrez, the CEO was David Crane and his big push for renewables and green energy. That led to his ouster, and Elliot’s first involvement with the spinoff of the NRG Yield renewables business. From your board perspective, how did that play out and why was the result maybe the best thing for NRG?

I don’t think the issue was being green. I think the issue at the end of the day was economic performance. When your stock falls precipitously and stays there for an extended period of time as a CEO, you must be very convincing to your investors that you have a plan to fix that. And, for better or for worse, that wasn’t the case for David. I know everyone thought it was a rejection of all things renewable, but I think it was a rejection of things unprofitable. I think we did a lot of really good things for a while and the next iteration under Mauricio, and then kind of hit another snag period. I think this has been the most interesting time to be at NRG because of the plethora of opportunities and the desire to play offense.

Getting back to the present, how do you see geopolitics with the tariffs, but also the emphasis on American energy dominance and where things stand today?

As opposed to yesterday or tomorrow? The problem is the instability. As a CEO, I can manage into any sort of criteria you give me. The hard thing is when you change it every day. From the power industry point of view, it’s a very strange time because we’re a very defensive stock. People still use power, and they actually spend more on smart homes and security when times are uncertain. And, yet, we have enormous growth potential. That’s a very rare thing to be a defensive stock with great growth potential. It’s usually one or the other. At the end of the day, I always believe that markets will determine what our energy policy is. I do think it will be somewhat tougher in some places for renewable folks if some of those benefits go away, but people will still be building renewables in places like Texas because they’re economical and an important part of the grid. I would welcome stability more than anything else but, at the end of the day, energy has always been determined by what people want and markets rather than what anybody’s been able to dictate as a policy.

On a personal basis, I’m curious about your background. You have more conventional economics and law degrees, but then you have a doctorate in archaeology. How did you end up going that route and how you got back to here?

I came out of law school and was an energy entrepreneur for a while. I was lucky enough to sell a couple businesses and kind of made a career switch and went back to do the PhD. I’d always loved archaeology. That’s what I did on vacations, go visit sites, visit museums. And, for the first time, I didn’t have a company I wanted to start. So, I went back to school. The worst thing that can happen is I hate it, and I quit. I obviously didn’t hate it. After a few years, in 2001 and 2002, there were a whole lot of energy bankruptcies. People were looking for people who were familiar with energy but hadn’t been involved in any of the bankruptcies. Well, I’ve been in graduate school. I ended up on two boards at that time, NRG and the other one was Enron International, called Prisma Energy post-bankruptcy. I always make sure I add that. The boards were great because I could go to meetings and still go to excavating sites. That’s what I was doing along with the [Escala Initiative] foundation that I started to help poor women entrepreneurs in Latin America that I had seen around my sites. And I was doing those three things right up until the day I got into this [CEO] seat.

This story was originally featured on Fortune.com