Don’t Reach Retirement Unprepared: 3 Questions You Must Answer Now If You’re in Your 40s or 50s

When it comes to saving for retirement, understanding exactly what you need to do to “be ready” to actually call it quits can be challenging. A number of factors go into this decision, including your own personal desire for when it is the right time to walk away. If you’re in your 40s or 50s […] The post Don’t Reach Retirement Unprepared: 3 Questions You Must Answer Now If You’re in Your 40s or 50s appeared first on 24/7 Wall St..

When it comes to saving for retirement, understanding exactly what you need to do to “be ready” to actually call it quits can be challenging. A number of factors go into this decision, including your own personal desire for when it is the right time to walk away.

There are three questions a pre-retiree needs to ask and have answered.

Always make sure you are working with a qualified financial advisor.

The hope is these questions get you to a good place financially to enjoy your golden years.

Are you ahead, or behind on retirement? SmartAsset’s free tool can match you with a financial advisor in minutes to help you answer that today. Each advisor has been carefully vetted, and must act in your best interests. Don’t waste another minute; get started by clicking here here.(Sponsor)

Key Points

If you’re in your 40s or 50s and haven’t started to think about some of the most important questions about retirement, there is no time like the present. The good news is that you still have time to get everything in order so you can walk away from the workforce whenever you feel it is the right time.

How Much Do I Need to Save, And Am I On Track With Retirement Contributions?

Knowing Your Retirement Number

This is a loaded question, as understanding your retirement number is no easy task. First, you must know exactly what lifestyle you hope to achieve in your golden years. Would you like to golf every week or travel to exotic places? Depending on the answer to this question and more, you can start thinking about how to calculate your retirement number.

The challenge is that you could be in trouble if you underestimate this number. The last thing you want is to be a few years into your retirement only to understand that you are running out of money faster than you think. This doesn’t mean you must be frugal now and put away more, but you must be aware of your special retirement number.

Tracking Progress

No matter what number you choose as your “magic” number for retirement, you must ensure you are tracking toward this. Let’s look at an example and consider that you might be behind where you should be with just $100,000 saved by turning 40, but you want to be at $1.5 million by the time you turn 65.

Knowing that you need to up your contributions, you’d have to consider the reality that you would need to start putting away around $30,000 annually, hoping it hits a 6% return yearly. Is this possible to achieve? This depends on your level of risk tolerance and working with the right financial advisor, but it is doable.

Lifestyle Changes

For better or worse, life happens, and when it does, it can be tragic, and it can mean a loss in the family, a job loss, or a new marriage. Any of these things can blow up the plans you have already made for retirement and force you to create a whole new plan. This new plan might require even more of a retirement fund to keep up your current lifestyle. The key here is that you must be very familiar with what changes are happening in your life and adjust your retirement number accordingly.

Are My Retirement Investments Appropriately Diversified?

Risk Versus Reward

Trying to balance risk versus reward while getting your chosen retirement number takes a certain level of confidence. Of course, the hope is that you are working with a financial advisor or on your own to create a diversified portfolio so that a single market downturn doesn’t set you back indefinitely. Let it be said that having a diversified set of investments will help you feel safer and sleep better, knowing that your money is stable.

Age And Goals

Knowing yourself in your early 40s and 50s, it’s really important to understand how these ages define your goals. It’s one thing if you are in your 60s and you want a portfolio that is more about being safe with your money. However, if you’re in your 40s, a financial advisor might recommend being a little more aggressive with growth stocks.

The last thing you want to do is work longer hours and more days when you’re in your 50s because you let your 40s fly by without being truly prepared. The hope is that you will have the type of success you need in your 40s and 50s by understanding the kind of investments you need to make.

Don’t Get Emotional

The last thing anyone can afford to be in the market is emotional, as you don’t want to get upset about either gains or losses. You want to make sure and avoid panic selling, which led millions of Americans to lose hundreds of thousands, if not millions, of dollars in investments during the Great Recession in 2008.

The same happened with the 2020 stock market fall caused by the COVID-19 pandemic. Far too many people sold at the bottom to avoid further losses, only for the market to recover a few months later. You have to be very disciplined to be invested, and it’s not everyone, but if you want to build a strong nest egg, you have to let your money work for you.

How Might Inflation Affect My Retirement Planning?

Purchasing Power

It won’t come as any surprise to learn that during periods of inflation, you will see the erosion of your purchasing power. Whether this is at the gas pump or the price of groceries as you check out, what $1 buys today is not what $1 will buy in 5, 10, or 15 years.

In other words, setting aside $30,000 today as a 40-something planning for retirement may later mean that you need even more money to keep up with inflation. This is precisely why you can’t avoid knowing exactly how much you need, as you should plan for things like a 2% or 3% inflation number that could wind up giving you a financial shortfall.

Savings Goals

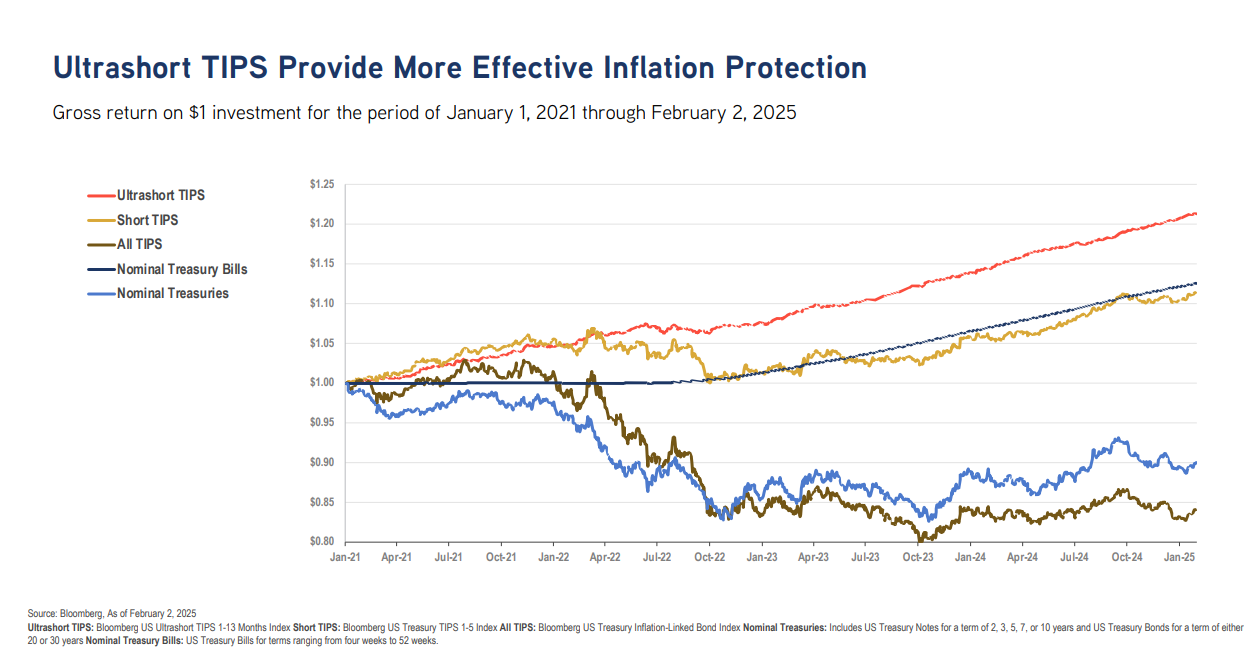

As unfortunate as it is to learn, you might need to look at the different investment opportunities available if you are well and truly worried about inflation. Stocks are good, but Treasury Inflation-Protected Securities are not as popular. However, they may be better for inflation than fixed-income accounts like CDs or high-yield savings accounts.

Here’s the honest truth: If you are 40 and want $1 million for retirement by age 65, you need closer to $1.8 million if inflation is averaging 3%. There is no telling if 3% is even the number you need to focus on, as inflation was 1.2% in 2020 but 8% in 2022, so it’s a bit like rolling the dice.

Healthcare Risks

Last but certainly not least, you must consider what healthcare risks can mean during retirement. You have to plan for the worst, like long-term healthcare needs that could cost upward of $100,000 a year in a living facility and unexpected medical bills that Medicare doesn’t cover 100%.

As unfortunate as it might be, medical costs are only going in one direction, and it isn’t down. This means you need to have a built-in buffer in case of additional medical costs so that you do not run out of money too fast.

The post Don’t Reach Retirement Unprepared: 3 Questions You Must Answer Now If You’re in Your 40s or 50s appeared first on 24/7 Wall St..