Two Social Security Policy Shifts That Could Change Your Benefits

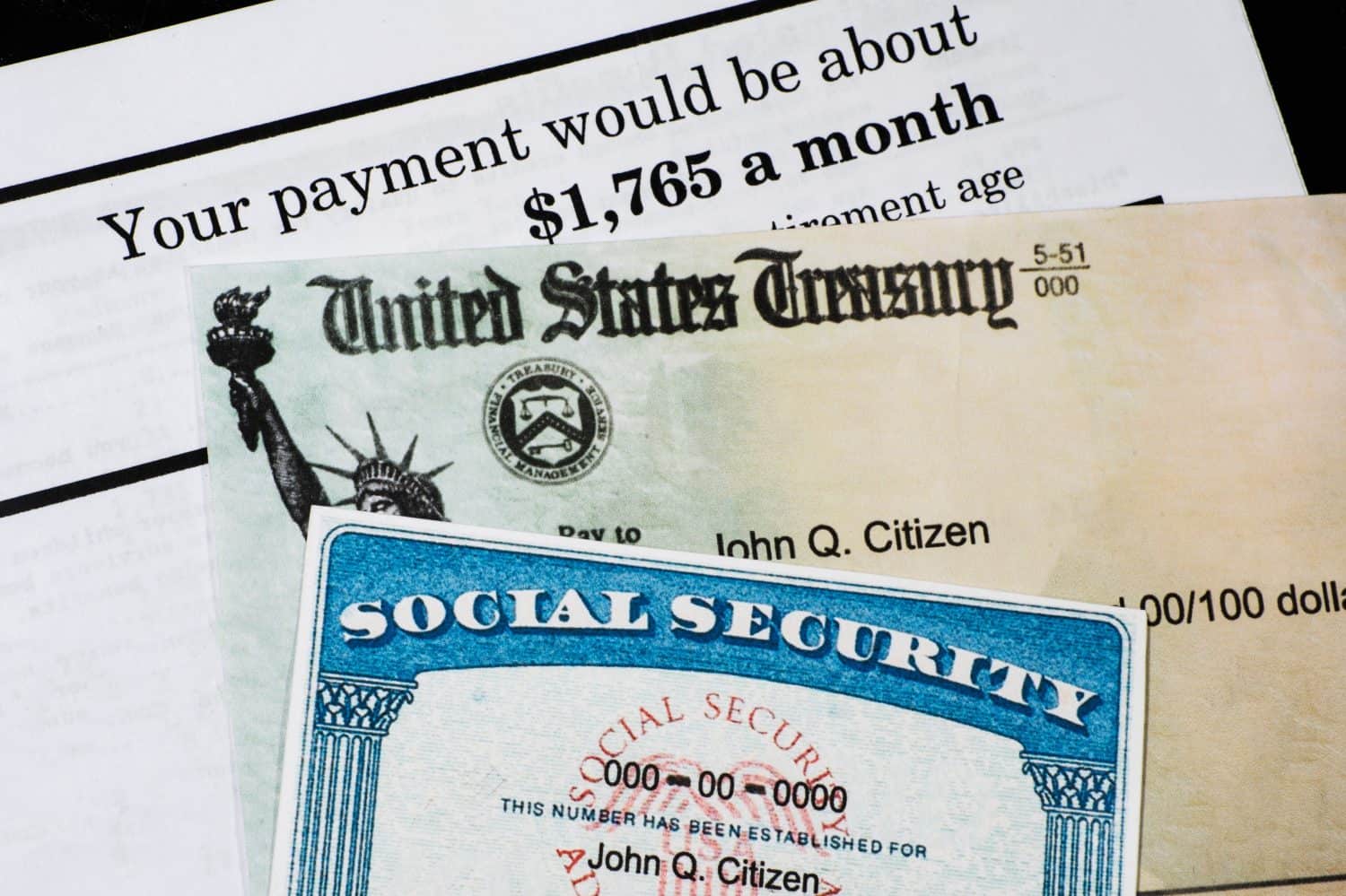

The typical retired worker on Social Security today collects about $2,000 a month. Some seniors get more, while others get less. But no matter how much money you’re getting from Social Security right now, let’s face it — you would probably appreciate getting more. And the good news is that if lawmakers take action, […] The post Two Social Security Policy Shifts That Could Change Your Benefits appeared first on 24/7 Wall St..

Key Points

-

Social Security is a lifeline for older Americans, but unfair policies routinely cost seniors money.

-

Adjusting the formula for COLAs could help seniors snag larger raises year to year.

-

Changing the rules for taxing benefits could put more money in seniors’ pockets.

-

Are you ahead, or behind on retirement? SmartAsset’s free tool can match you with a financial advisor in minutes to help you answer that today. Each advisor has been carefully vetted, and must act in your best interests. Don’t waste another minute; get started by clicking here.(Sponsor)

The typical retired worker on Social Security today collects about $2,000 a month. Some seniors get more, while others get less.

But no matter how much money you’re getting from Social Security right now, let’s face it — you would probably appreciate getting more. And the good news is that if lawmakers take action, it could pave the way to larger benefits. Here are two policy changes that could put more money in seniors’ pockets.

1. A new COLA formula

Inflation has a tendency to drive living costs up from one year to the next. That’s why lawmakers implemented a rule decades ago that makes Social Security benefits eligible for an automatic cost-of-living adjustment (COLA).

It used to be that COLAs had to be voted in for Social Security benefits to go up. Now, lawmakers don’t need to meet for that to happen.

But there’s a problem with the formula used to calculate Social Security COLAs. And as a result, seniors have lost out on buying power through the years.

Social Security COLAs are based on an index called the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). But there are problems with using this measure.

For one thing, notice how the index refers to wage earners and clerical workers? Many Social Security recipients are, by nature, retired and not working. That’s the first disconnect.

The second issue is that many Social Security recipients reside outside of urban areas. And that could lead to different expenses.

All told, the CPI-W is not an index that’s reflective of the costs American retirees face regularly. Because of this, it’s not the best measure for calculating Social Security COLAs.

If lawmakers were to shift to a senior-specific index, it could result in larger COLAs. That could, in turn, help more retirees on Social Security better manage their expenses.

2. A new combined income formula

As part of his campaign, President Trump pledged to eliminate taxes on Social Security benefits. But taking away that revenue stream could push Social Security closer to insolvency. So it’s unclear as to whether that change will actually happen. But one change that may be possible is a new formula for combined income.

Combined income is the formula used to determine if seniors on Social Security get taxed on their benefits. And it’s calculated as follows:

- 50% of your annual Social Security income

- Annual adjusted gross income (AGI)

- Annual tax-free interest income

Here’s how that might work. Say you get $48,000 a year from Social Security, have an AGI of $30,000, and have no tax-free interest income you collect. Your combined income would total $54,000.

Here’s the problem, though. If you’re single, a combined income of $25,000 or more means you’re taxed on your Social Security benefits. If you’re married, this threshold rises to 32,000.

But either way, retirees don’t get a lot of leeway to earn a decent income without putting their Social Security benefits at risk of getting taxed. So while Trump may not succeed at eliminating taxes on Social Security, what may happen is that lawmakers make changes to the combined thresholds so that they increase and become more aligned with inflation.

Or, lawmakers could make changes to what goes into the formula. For example, they could base combined income on AGI and tax-free interest income only, taking Social Security income out of the equation. That would likely help retired Americans hang onto more of their benefits.

The post Two Social Security Policy Shifts That Could Change Your Benefits appeared first on 24/7 Wall St..