Treasury Secretary Bessent blames Trump tariff sell-off in markets on deflating AI bubble—‘that’s a Mag 7 problem, not a MAGA problem’

Bessent appears to be more interested in bringing down borrowing costs to stave off a potential sovereign debt doom loop than in the $1.5 trillion drop in equities.

- U.S. equity markets lost roughly $1.5 trillion after President Trump announced sweeping punitive import duties, but the administration is more interested in bringing down borrowing costs to stave off a potential sovereign debt doom loop.

When President Donald Trump hoisted a spreadsheet listing all the punitive tariffs he planned to levy on the rest of the world late Wednesday, investors had one thing in mind—bolt for the exits.

Futures contracts on the S&P 500 and the Nasdaq 100 dropped sharply once markets learned that starting next week the U.S. will hit goods from China with an additional 34% duty, not to mention 20% on those from the European Union and 24% on those from Japan. Former Harvard economist Lawrence Summers calculated roughly $1.5 trillion in market value was wiped out in the course of about an hour.

Despite being able to trace the equities futures sold off to this moment, administration officials dismissed the afterhours movement and instead blamed the stock prices slump on DeepSeek, the open source AI model from China that punctured tech valuations in January.

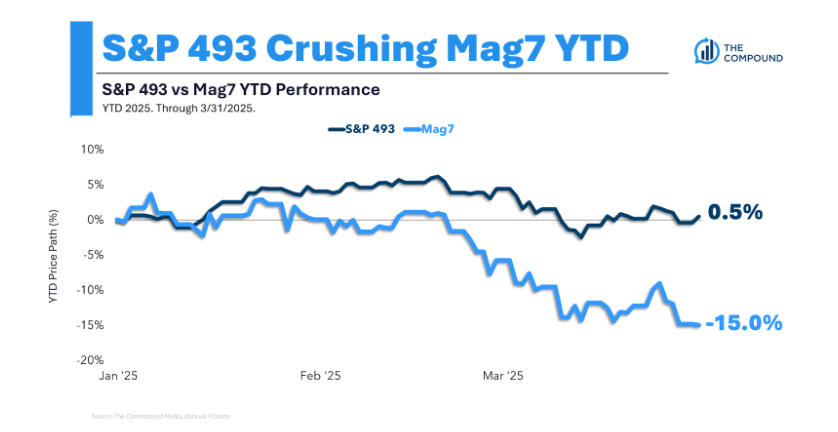

“What I would point out is that the Nasdaq peaked on DeepSeek day,” Treasury Secretary Scott Bessent told Bloomberg TV on Wednesday. “So that is a MAG-7 problem, not a MAGA problem.”

Not true, says Saxo Bank’s global head of investment strategy, who traced bearish sentiment in everything from Amazon to Nike to a once-in-a-century hike that lifts the average effective import duty by nearly 19 percentage points.

“In what President Donald Trump labelled a ‘Liberation Day’ for the American economy, April 2nd saw the unveiling of the broadest and most aggressive tariffs imposed by the United States in over 100 years,” wrote Jacob Falkencrone on Thursday. “Markets around the globe reeled in response.”

Debt refinancing tsunami

Bessent’s reaction may not simply be an attempt to avoid uncomfortable questions about the S&P 500 index hitting six month lows. There are other reasons why the White House might want to deflect voter attention away from equity markets.

The former hedge fund manager has said he wants the new litmus test for the health of the U.S. economy to be the benchmark 10-year Treasury bond, from which the larger credit market—including car loans and home mortgages—is broadly priced.

The lower its yield, the more affordable it becomes to borrow money both for Americans and Uncle Sam. That’s key as Bessent inherits from his predecessor a crisis that Wall Street veterans including Stanley Druckenmiller blasted as tragically myopic.

The Biden administration’s decision to roll over much of its debt using notes with short-term maturities like Treasury bills now means there’s a tsunami of debt that Bessent’s department needs to refinance this year without breaking the bank in the process.

Preventing a U.S. debt market doom loop

Interest payments on the national debt have already eclipsed annual defense spending, hitting $1 trillion last year. A significant rise from the current level could trap the U.S. in a doom loop where it has to borrow more and more money at increasingly higher rates just to service its debt.

Trump and Bessent have made it clear they aim to prevent that vicious circle by pushing down borrowing costs on long bonds, the part of the yield curve over which the Federal Reserve has little control. While this may be hurting stocks in the short term, the alternative could be far worse.

Billionaire investor Ray Dalio, founder of the macro hedge fund Bridgewater, has given policymakers three years at most to fix the mounting U.S. debt problem before they risk seeing a buyers strike the next time they try to issue sovereign bonds.

So far Bessent’s plan appears to be working. Spooked by Trump’s punitive across-the-board tariffs, markets are pricing in the growing possibility of a recession.

Alongside buying gold, investors have piled into U.S. debt, pushing the 10-year from 4.80% down to 4.08% in less than three months.

This story was originally featured on Fortune.com