How Baby Boomers Can Retire Ahead of Schedule Without Living Like a Hermit

This post may contain links from our sponsors and affiliates, and Flywheel Publishing may receive compensation for actions taken through them. Baby Boomers are retiring by the millions. In fact, 11,200 Americans will turn 65 every day – or about 4.1 million a year – from 2024 to 2027, as noted by CNBC. Unfortunately, according […] The post How Baby Boomers Can Retire Ahead of Schedule Without Living Like a Hermit appeared first on 24/7 Wall St..

Baby Boomers are retiring by the millions.

In fact, 11,200 Americans will turn 65 every day – or about 4.1 million a year – from 2024 to 2027, as noted by CNBC. Unfortunately, according to AARP, about 52.5% of them have less than $250,000 in retirement assets and may have to rely on Social Security as income.

Key Points About This Article

- If you want to comfortably retire, start by having a conversation with a financial advisor.

- Max out your retirement accounts, such as your 401(k).

- Make sure you have an emergency fund, and be sure to budget and plan ahead.

- Also: Take this quiz to see if you’re on track to retire (Sponsored)

“America has never seen so many people reaching retirement age over a short period, and well over half of them will find it challenging to meet their needs through their retirements, let alone maintain their current standard of living,” Robert Shapiro, a former U.S. undersecretary of commerce and lead author of the study, said, as quoted by AARP. “They lack the protected income that many older boomers have from solid pensions or higher savings.”

Of course, none of us want to find ourselves in such a situation.

All of which highlights the importance of saving and speaking with a financial advisor.

So, what’s the best way to retire ahead of schedule without living like a hermit?

There are several key ways.

The top one is to have a conversation with your financial advisor. This person can best guide you on the key steps you should take to retire comfortably or help fix your current situation.

Two, with your advisor, create an in-depth retirement plan.

That includes current income sources, such as Social Security, pensions, investments, and retirement plans. It should also include projected expenses such as taxes, and money set aside for unexpected events, as compared to expected income numbers.

As you near retirement, “begin with the end in mind,” as noted by Stephen Covey, author of The 7 Habits of Highly Effective People.

That includes the consideration of how much you need to spend every year on rent or mortgage unless you’re one of the lucky ones who have paid off your mortgage, healthcare and long-term costs, groceries, medication, transportation costs, and perhaps even pet expenses. Plus, do you expect to travel a lot, and how much do you foresee spending? Maybe you have plans to help your children, and even their children with things such as college tuition.

Three, save aggressively. Max out your retirement accounts, such as your 401(k).

If you have an employer that will match your 401(k), maximize your contributions up to the amount your employer will match. If your employer will match up to 6% of your salary, maximize that.

To really build your wealth using that employer match, start early with your employer, even if you can only afford to invest 1% of each check into retirement. If you earn $75,000 a year and you contribute 1%, that’s $750 for retirement. Also, if your employer matches that, you have $1,500 for retirement per year. If you contribute 6% and your employer matches that, that’s about $6,750 in retirement per year.

Fourth, follow the 4% retirement rule.

Let’s say you want to earn at least $75,000 per year in your retirement. Following the 4% rule, you need a nest egg of about $1.875 million. That rule suggests that if you withdraw 4% from your retirement each year, it should last you about 30 years. For example, if you want or need $50,000 per year, your nest egg should be about $1.25 million. For $75,000, your nest egg should be about $1.87 million.

Five, delay Social Security if you can.

Choosing the right time to retire and to receive retirement benefits is essential.

While that can depend on variables such as a shortfall in retirement savings, health, current income, and other financial needs, a delay in receiving social security can be beneficial.

According to the Social Security Administration, “If you have reached full retirement age, but are not yet age 70, you can ask us to suspend your retirement benefit payments. By doing this, you will earn delayed retirement credits for each month your benefits are suspended which will result in a higher benefit payment to you.”

According to Kiplinger.com, “For every year you delay taking your Social Security benefits past full retirement age, you get a bump of 8% in your benefit until age 70. For example, if you’d receive $1,000 per month at your full retirement age of 66, delaying your benefits to age 70 would boost your monthly check to $1,320.”

Six, make sure you have an emergency fund.

Let’s say you were involved in a terrible accident and you can’t work. Unless you have a catastrophic insurance policy, you and your family should have at least eight months’ worth of living expenses saved through that rough period, according to finance coach, Suze Orman.

For many of us, saving eight months of expenses is easier said than done.

If you can’t swing that, start small with an emergency savings goal of at least $1,000. Sure, it’s small but it’s a safety net, and it’s a start. If you can put away about $85 a month, you’ll reach that goal and have some wiggle room.

However, be sure to store this in a separate “don’t touch” account, automatically depositing money every time you’re paid. Plus, if you ever receive another source of income, such as a bonus or a gift, put it directly into that “don’t touch” account instead of spending it immediately.

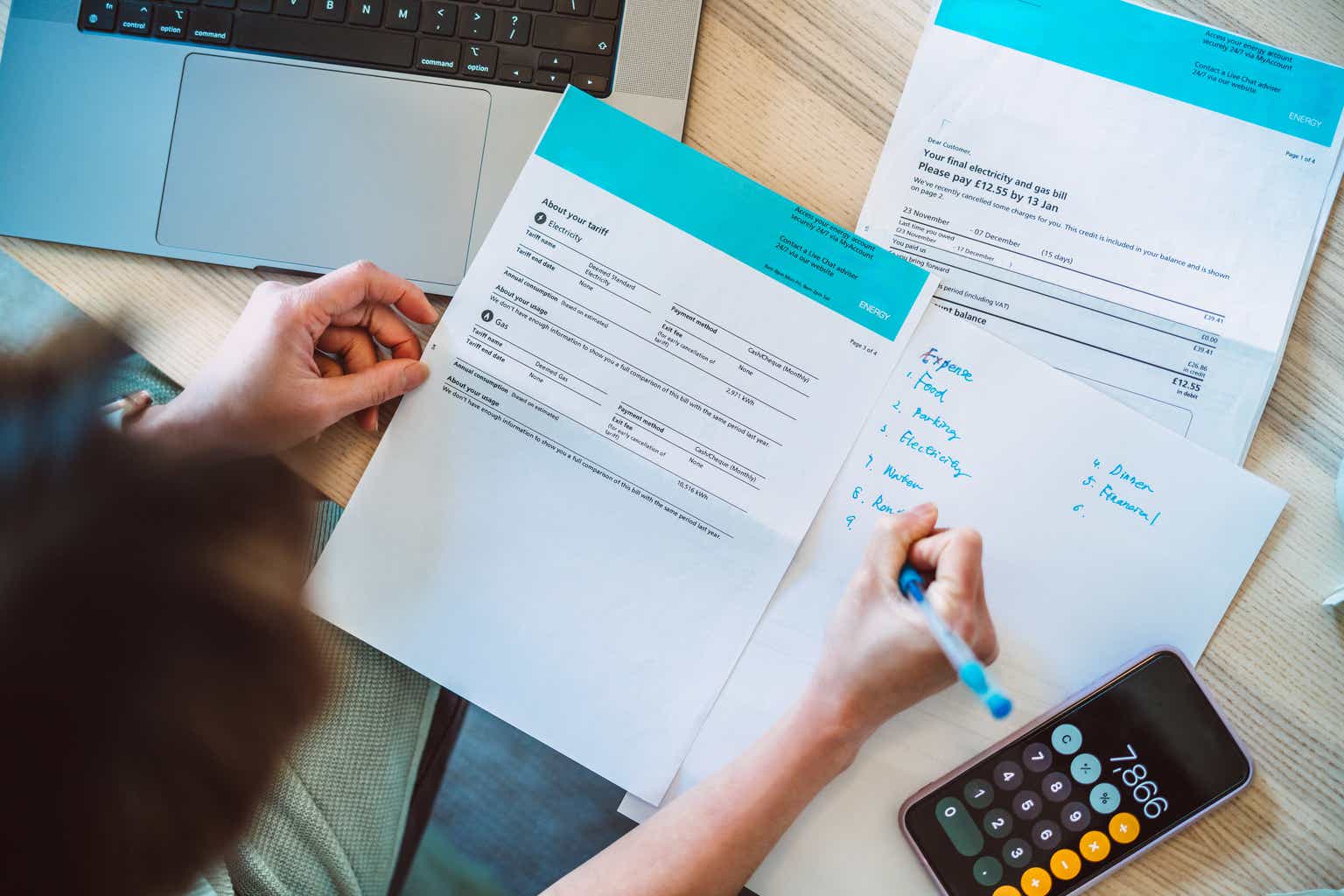

Seven, budget and track your expenses.

This is crucial. Without a budget, many of us lose account of what’s coming in financially and what’s going out.

When others have asked me for financial advice, my top question is, what are you spending on? Unfortunately, I’m often met with the deer in the headlights stare and a response of “I don’t know.”

And, unfortunately, not knowing will destroy you financially and could possibly damage your retirement plans.

The post How Baby Boomers Can Retire Ahead of Schedule Without Living Like a Hermit appeared first on 24/7 Wall St..