Do These 3 Things to Beat the Average American’s 401(k)

There are many retirees today who have to pay their bills on Social Security alone. And people in that boat tend to struggle financially, and for good reason. Social Security only pays the average retiree today about $2,000. If the idea of living on $24,000 a year doesn’t sound appealing to you, then it’s important […] The post Do These 3 Things to Beat the Average American’s 401(k) appeared first on 24/7 Wall St..

Key Points

-

It’s important to have savings for retirement so you don’t struggle to pay the bills.

-

Saving from a young age can help you beat the average 401(k) balance.

-

It’s also important to invest your money shrewdly.

-

Are you ahead, or behind on retirement? SmartAsset’s free tool can match you with a financial advisor in minutes to help you answer that today. Each advisor has been carefully vetted, and must act in your best interests. Don’t waste another minute; get started by clicking here.(Sponsor)

There are many retirees today who have to pay their bills on Social Security alone. And people in that boat tend to struggle financially, and for good reason.

Social Security only pays the average retiree today about $2,000. If the idea of living on $24,000 a year doesn’t sound appealing to you, then it’s important that you do what you can to save well for your senior years. And if you have access to a 401(k) plan through your job, you might as well take advantage of it.

Vanguard reports that the average 401(k) balance today is $134,128. That average, however, is across all age groups.

Older workers do have more money saved for retirement than their younger counterparts. But if you want to beat the average 401(k) balance, there are three critical things you should do.

1. Claim your full workplace match

It’s common for employers to offer a match in their 401(k) plans as an employee benefit. So if that’s an option for you, it pays to take advantage of it.

Not only is a 401(k) match free money for your retirement, but it’s also money from your employer you can invest. To put it another way, your employer might give you $3,000 for your 401(k) this year if you contribute at least that much. But over 30 years, that $3,000 could grow into $30,000 or more, depending on how your 401(k) performs.

2. Start funding your account at a young age

The more time you give the money in your 401(k) to grow, the larger a balance you’re likely to end up with. So it pays to start funding your 401(k) as soon as you can.

You may not be able to do that your first year out of college or even your fifth, especially if you’re saddled with student loan debt like so many graduates are. But if you can manage to begin saving for retirement in your 20s, you could end up with a very large 401(k) balance by your 60s.

Let’s say you start contributing $200 a month to your 401(k) at 29 and you retire at 65, giving yourself a 36-year savings window. If you score an 8% yearly return in your 401(k), which is a little bit below the stock market’s average, you could end up with about $449,000.

Not only does that beat the average 401(k) balance today, but it’s also more than what the average saver aged 65 and over has ($272,588), according to Vanguard.

3. Invest your savings wisely

Keeping your 401(k) in cash is one of the biggest mistakes you can make. If you want a large balance, make a point to invest that money so it grows steadily.

The example above showed what might happen with an 8% return each year in your 401(k). If you play it too safe, you won’t get a return that high.

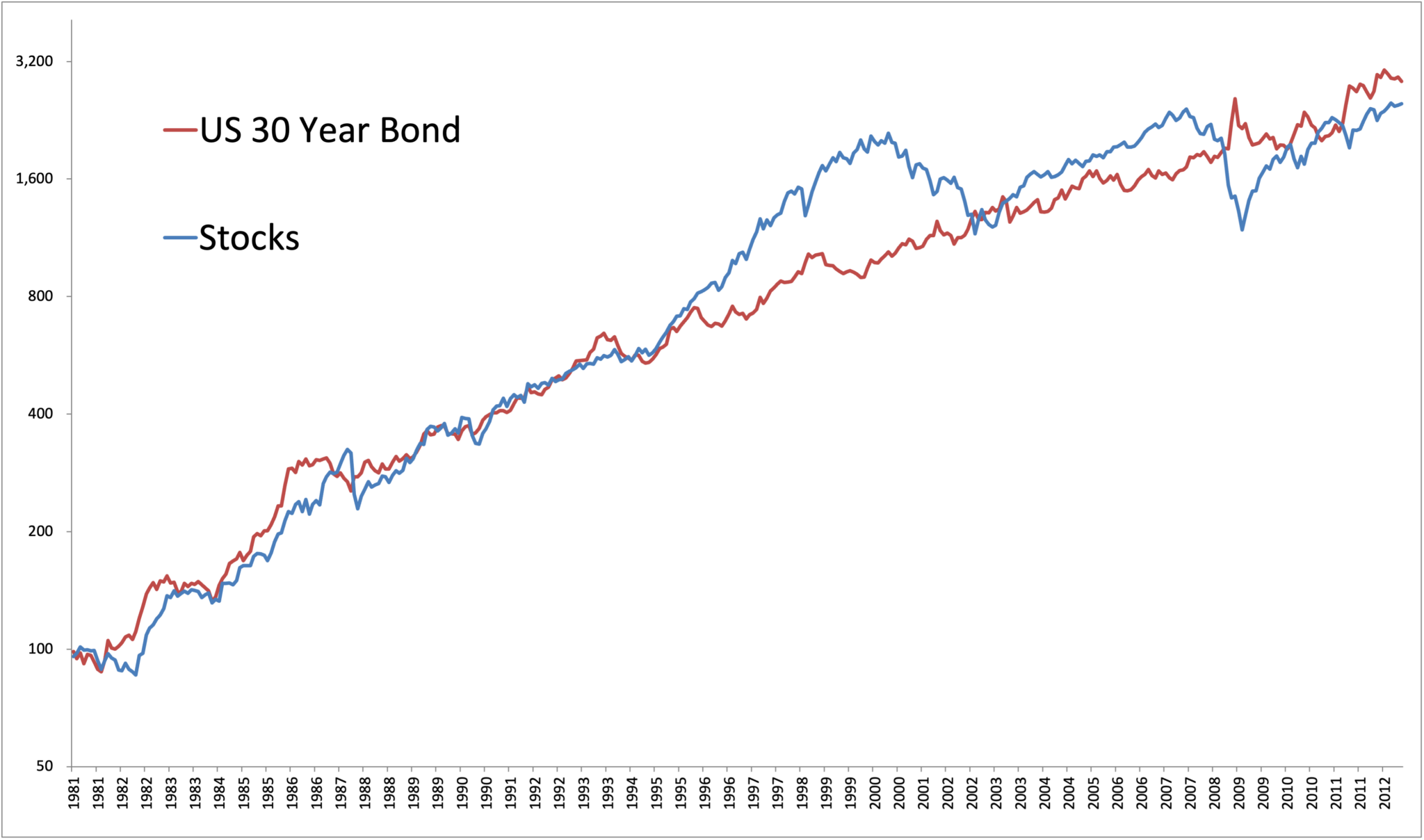

A good bet for a 401(k) is to seek out low-cost S&P 500 index funds. Because these funds aren’t actively managed, their fees tend to be low. At the same time, you can benefit from the performance of the stock market to grow your savings — and hopefully lead you to a large balance you’re happy with.

The post Do These 3 Things to Beat the Average American’s 401(k) appeared first on 24/7 Wall St..