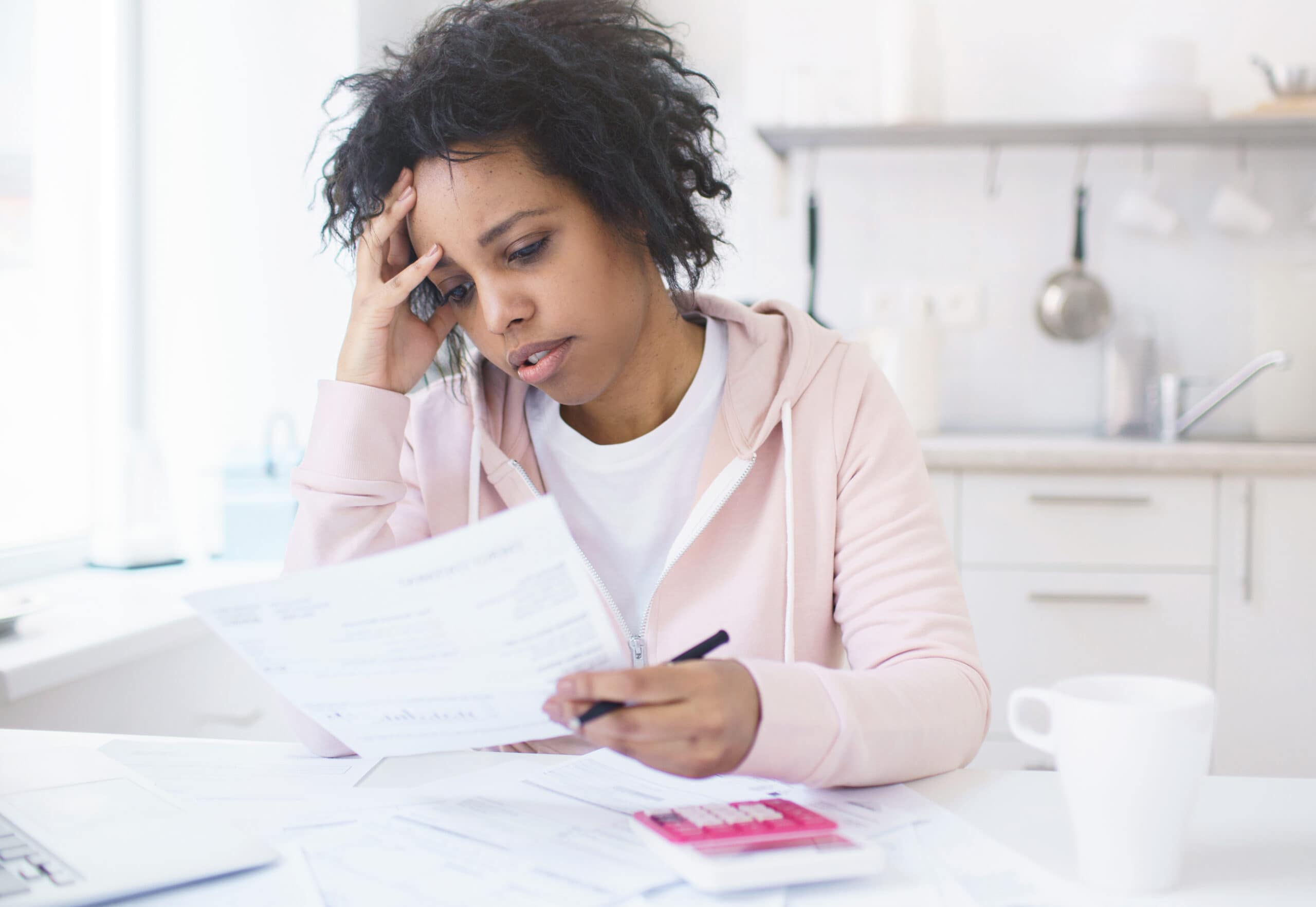

My Mother Ruined My Credit Score – How Can I Fix It Before Buying a House?

Unfortunately, as soon as your credit falls below a certain level, challenges can mount, not only with how to get it back up but also with what limitations a low credit score can result in. Perhaps the biggest challenge is that far too many people don’t have the right financial habits to dig out of […] The post My Mother Ruined My Credit Score – How Can I Fix It Before Buying a House? appeared first on 24/7 Wall St..

Unfortunately, as soon as your credit falls below a certain level, challenges can mount, not only with how to get it back up but also with what limitations a low credit score can result in. Perhaps the biggest challenge is that far too many people don’t have the right financial habits to dig out of any credit holes.

This Redditor is in a regrettable situation, and his mother has knowingly done this to him.

There is no question that the Redditor has a long road to recovery in terms of his credit score.

The best-case scenario is to sell the car and pay it off completely, which will start the clock on repairing his credit.

The right cash back credit card can earn you hundreds, or thousands of dollars a year for free. Our top pick pays up to 5% cash back, a $200 bonus on top, and $0 annual fee. Click here to apply now (Sponsor)

Key Points

This is precisely the case with one Redditor posting in r/personalfinance, who is just learning how bad his mother is with her credit and money. Making matters worse, his mom’s poor behavior is now directly affecting his credit, and he’s unsure how to move things in the right direction.

Mother Ruins Credit

In this story, the 25-year-old Redditor highlights that he should have seen the warning signs when he was 18, when his mother had him cosign on a car. At the time, she told him it was to “kickstart his credit,” but he now realizes it was because her credit was so terrible.

The mother, 52, is what the son calls “the worst with money” he has ever seen, and is currently dealing with the fallout of learning this. He’s already had to help her get her car back after it’s been repossessed twice, and one of these situations cost him $2,200 of his own money.

Making this whole story worse is that while he’s navigating the likelihood that her car will be repossessed again, his mom went to Rent-A-Center and got a Ninja Air Fryer for herself. For someone with 0-5% in credit card debt, the mother’s behavior is taking her son’s excellent credit score of 700+ down to a 580.

Understandably, the son is now trying to figure out what, if anything, he can do to resolve this situation. First and foremost, he needs to detach himself from everything his mom is doing credit-wise, and for that, he wonders if he needs some kind of credit lawyer.

Challenges Ahead

As far as the car goes, there is very little the original poster can do short of paying for the loan himself. As a co-signer, he is legally responsible for the debt, and if the car is repossessed a third time, it will drop his already low 580 credit score even further. Car companies and debt collectors don’t care about the situation, they want to collect money, so explaining everything won’t help.

As far as contacting a lawyer, this likely isn’t the helpful scenario the original poster hopes it would be. He’s legally on the documents for the car loan, and at 18 years of age, it’s going to be hard to claim that he didn’t know what he was signing for or why.

The bottom line regarding the car loan is that he is stuck, which means the best scenario might be to let the car get repossessed and then go from there. Some financial negotiation might be available after the bank has taken possession of the vehicle, as the bank will want at least some money back. Of course, the most important thing is that the son must stop bailing mom out, even at the risk of his credit. He’s still young enough that he has time to repair it before it becomes irreparable, so that is the good news.

The bad news is that for now, the son took his mother’s word that she could handle the car payment and has learned a hard and valuable lesson. The only other alternative is to consider selling the car and using whatever money is received to pay off as much of the balance as possible and then pay for the rest. However, with mom being a co-signer, there has to be mutual agreement on this step.

Seven Years Ahead

The only good news here is that under the Fair Credit Reporting Act, negative information is removed from your credit report once the car situation is resolved. In the meantime, getting a mortgage or even renting an apartment will be pretty challenging, which is an unfair consequence of the original poster trusting his mom to do the right thing with the car payment.

The only real way to fix this and start rebuilding credit is to figure out the car situation, as it’s the only real hindrance to a future home purchase. Outside of the vehicle, there isn’t much more the Redditor can do to speed up the credit repair.

The post My Mother Ruined My Credit Score – How Can I Fix It Before Buying a House? appeared first on 24/7 Wall St..